Financial News Highlights

- An upside inflation surprise didn’t do much to move markets, as the details of the report fell in line with expectations in financial news.

- The focus remains firmly on the services sector, where housing costs continue to prop up price growth.

- Looking forward, the Fed will need to see more consistent evidence of disinflation – likely delaying any policy changes to mid-year.

The Long and Bumpy Road

Taming inflation is never easy, and usually proceeds in fits and starts in financial news. So, given the experience of the past year, this week’s hotter-than-expected print to consumer price index (CPI) inflation doesn’t come as all that much of a surprise. Indeed, the details of the report left room for optimism and meant that markets brushed off the surprise – leaving ten-year U.S. treasury yields virtually unchanged on the news. The positive developments under the hood (so to speak) fell in line with consensus expectations and meant that the focus could be kept firmly on the timing of possible Fed cuts.

Taming inflation is never easy, and usually proceeds in fits and starts in financial news. So, given the experience of the past year, this week’s hotter-than-expected print to consumer price index (CPI) inflation doesn’t come as all that much of a surprise. Indeed, the details of the report left room for optimism and meant that markets brushed off the surprise – leaving ten-year U.S. treasury yields virtually unchanged on the news. The positive developments under the hood (so to speak) fell in line with consensus expectations and meant that the focus could be kept firmly on the timing of possible Fed cuts.

Headline CPI inflation rose 0.3% month-on-month (m/m), taking the annual reading for December to 3.4%. While the print did exceed market expectations, it was the more closely watched core measure that drove the muted market response. The price index excluding food and energy matched the headline gain at +0.3% m/m – a pace it has logged in four of the past five months. This is the interesting bit, on a three-month annualized basis core CPI inflation is running at 3.3%, roughly unchanged since October and still clear of the Fed’s target.

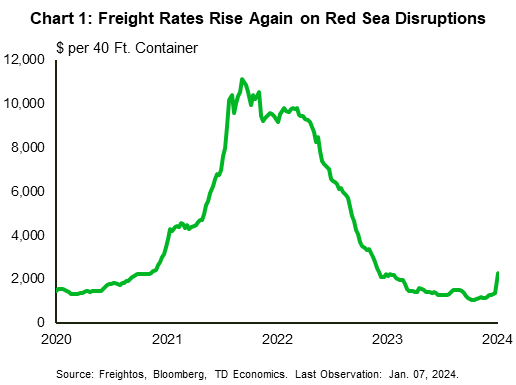

The stickiness in the core measure is slightly concerning, particularly as core goods prices remained flat, snapping a six-month run of price declines. Moreover, there is some near-term upside risk to goods prices as attacks on ships in the Red Sea affecting access to the Suez Canal have lead to a jump in freight costs (Chart 1). Despite this, what the pause in goods price deflation laid bare was the ongoing strength in services price gains.

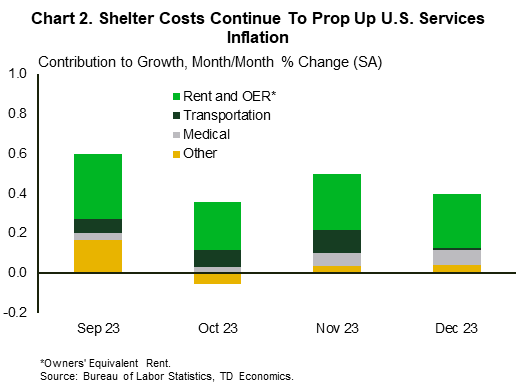

Core services prices were up 0.4% m/m in December. Moreover, the strong price gains have been persistent, with the three-month and six-month (annualized) rates of core services inflation at 5.1% and 5.2%, respectively. Yet, while these figures are significantly higher than the Fed would feel comfortable with, there are reasons to believe conditions are improving. Currently, the largest contributing factor to services inflation is the shelter component (Chart 2). On this front relief is expected as increases in observed rents (which tend to lead the measure in the CPI report)  have moderated sharply in recent months – a dynamic that is still gradually working through to the shelter component of CPI. Moreover, the slowdown in home price appreciation through early-2023 also continues to gradually work its way into the CPI.

have moderated sharply in recent months – a dynamic that is still gradually working through to the shelter component of CPI. Moreover, the slowdown in home price appreciation through early-2023 also continues to gradually work its way into the CPI.

The return to two percent inflation continues to be bumpy, but progress has been tangible and signs suggest that the Fed continues to be on course. After a few months of solid progress, optimism had begun to emerge that cuts might come sooner rather than later. However, price pressures remain sticky, and the economy continues to outperform. December job growth was above trend, and the Atlanta Fed Nowcast is expecting GDP growth of over 2% (annualized) in the fourth quarter or 2023.

A packed slate of Fed speakers is on tap for next week, and should hopefully give some additional insight into how they view the recent data. However, given this week’s developments, it will likely be mid-year before officials have sufficient evidence signs that they can begin loosening their policy stance.

Andrew Hencic, Senior Economist | 416-944-530

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.