Financial News Highlights

- The Federal Reserve held the policy rate steady this week and signaled that rates will likely remain higher for longer in financial news.

- The U.S. jobs engine slowed in April, adding 175k jobs. The unemployment rate rose modestly to a still low 3.9%.

- Last year’s productivity surge has come to an end. Productivity growth slowed to a stall speed in Q1, while unit labor costs turned sharply higher.

Holding Steady for Longer

It was a very busy week on the economic data calendar, but the two headliners were a pulse check on the state of the labor market and the Federal Reserve’s interest rate announcement in financial news. Policymakers delivered no surprises this week, with the FOMC voting unanimously to hold the policy rate steady at the current target range of 5.25% – 5.5%. The same can’t be said for April’s employment report, which showed job growth coming in handily below expectations. Financial markets greeted the news positively, with the S&P 500 recouping its losses from earlier in the week, while the 10-year Treasury yield was down 14-bps to 4.53% at the time of writing.

It’s not that long ago that investors were expecting the first rate cut to come at this very meeting. But after three months of hotter-than-expected inflation readings, the FOMC appears to be on hold indefinitely, as it looks for “greater confidence that inflation is moving sustainability back towards 2%”. What exactly that means remains to be seen, but it will likely require a further rebalancing in the labor market, which ultimately leads to more sustained downward pressure on wage growth.

From that perspective, April’s jobs data was a Goldilocks report. Non-farm payrolls rose by 175k while the unemployment rate ticked up to 3.9%. Importantly, average hourly earnings cooled more than expected, with the 12-month change slipping to a near three-year low of 3.9% (Chart 1).

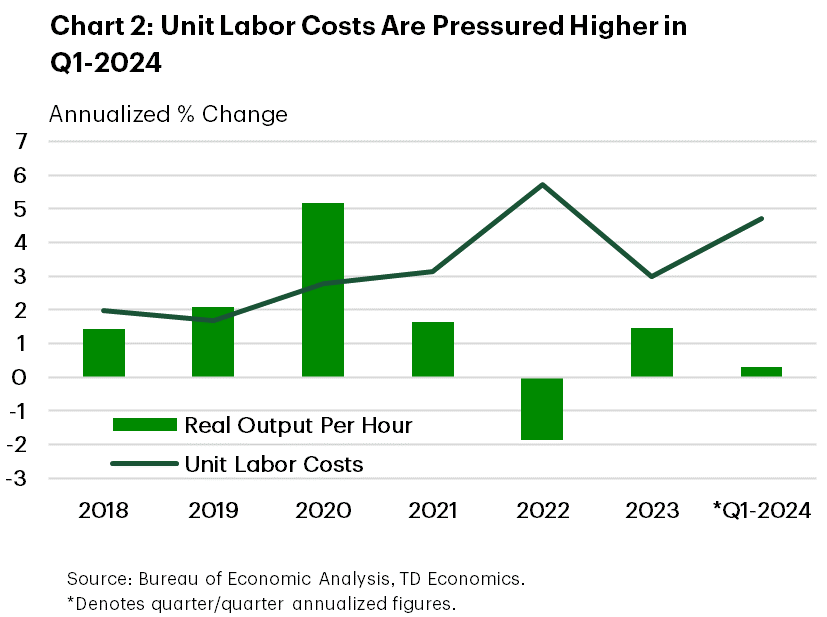

While the softening in wage growth will come as welcome news for Fed officials, it needs to be weighed against other measures of employee compensation, particularly the Employment Cost Index – the Fed’s preferred wage measure – which showed an unexpected acceleration. Moreover, after rising by a robust 1.5% in 2023, growth in non-farm productivity slipped to a near stall speed in Q1. Taken alongside last quarter’s uptick hourly compensation, unit labor costs (ULC) also rose sharply higher (Chart 2). This has important implications for inflation. ULC can best be thought of as a productivity adjusted cost of labor, making it a useful gauge on the extent to which the nominal pace of compensation growth is running above (or below) what would be consistent with achieving 2% inflation. However, with the Q1 reading not only turning higher but also running at an annualized rate that’s more than double where it should otherwise settle, provides yet another signal that progress on the inflation front has indeed stalled.

In the press conference following the release of the FOMC statement, Chair Powell noted that while ongoing progress is “not assured” he still expects that over the course of the year “inflation will move back down”. But Powell also emphasized that he’s become less confident in that forecast. Moreover, when asked if today’s rates were “sufficiently restrictive” Powell instead described them as only “restrictive”. While the Chair said further rate hikes are “unlikely”, the refusal to characterize today’s stance as sufficiently restrictive is an implicit acknowledgment that further policy firming cannot be ruled out. At this point, we view this as highly unlikely. But given the economy’s sustained strength alongside the recent stalling on inflation, we now expect the Fed to remain on hold until December.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.