Financial News Highlights

- The Federal Reserve Senior Loan Officer Opinion Survey showed that most banks tightened lending standards further in the first quarter, with demand for loans falling in concert in financial news.

- Growth in U.S. consumer credit slowed materially in March as the upward trend in rates through the first quarter weighed on volumes.

- Federal Reserve officials reiterated their expectations that interest rates would need to remain higher for longer to ensure inflation returns sustainably to their 2% target.

Credit Conditions Tighten as Fed Remains Vigilant

After last week’s Federal Reserve decision and employment report, the second week of May was comparatively lighter on data releases. First quarter reports for lending activity and consumer credit showed that tighter lending standards continue to weigh on credit demand. However, financial markets were more attentive to the comments of Federal Reserve officials as they sought insights on the potential path of monetary policy moving forward. As of the time of writing, the S&P 500 was up 2.1% on the week, while Treasury yields were roughly unchanged.

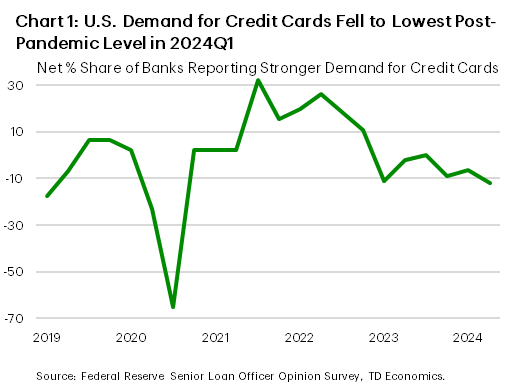

Starting things off on Monday, we received the updated Federal Reserve Senior Loan Officer Opinion Survey (SLOOS) for the first quarter. Survey responses showed that banks continued to tighten lending standards and report weaker demand for loans across all business and consumer loan categories. Relative to the fourth quarter of 2023, more banks tightened lending standards for consumer credit, fewer tightened commercial and residential real estate credit, and roughly the same number of banks tightened commercial & industrial credit in financial news. Within consumer credit, tighter lending standards pushed the net share of banks reporting stronger demand for credit cards to its lowest level since mid-2020 (Chart 1).

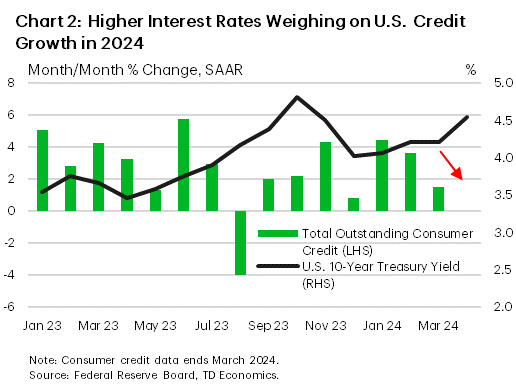

Looking at the monthly breakdown for consumer credit, the March data showed consumer credit growth decelerated considerably through the first quarter as interest rates trended higher (Chart 2). While consumer credit still expanded 3.2% (annualized) in the first quarter, the gains were largely front-loaded in the earlier months and tapered off as financial conditions tightened. With interest rates continuing to push higher through the first half of the second quarter, it seems likely that a further softening in consumer credit growth will occur over the coming months. Combined with depleted pandemic excess savings, weakening consumer credit growth is expected to lead to moderating consumption growth in 2024. While this should aid the Federal Reserve in their attempts to return inflation to their 2% target, officials emphasized their vigilance in recent remarks.

Vice Chair and New York Fed President John Williams noted this week that monetary “policy is in a very good place, and we have the time to collect more [data], so steady as she goes”. This sentiment was echoed by Richmond Fed President Barkin who stated his optimism that “today’s restrictive level of rates can take the edge off demand in order to bring inflation back to our target”. Most members noted that they did not expect further policy tightening to be necessary, with Minneapolis Fed President Kashkari stating that “the bar for us raising is quite high, but it’s not infinite”. While the prospect for higher rates is unlikely at this time, Fed officials are expected to remain vigilant against the potential for upside risks to inflation.

April’s Consumer Price Index report next week will offer the next barometer on inflation trends as the Fed prepares to update their Summary of Economic Projections ahead of their next meeting on June 11-12th.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.