Financial News Highlights

-

- Revisions to economic growth in the first quarter featured a mark down to consumer spending in financial news.

- That theme continued in April, where a contraction in real personal consumption expenditures came as a confirmation that restrictive rates are working.

- Inflation also took another step in the right direction. But sticky services inflation still has room to fall before the Fed can feel confident that inflation has been tamed.

A Slight Downshift

Bond yields are climbing down from this week’s highs as a pair of high-profile data releases suggest the some of the steam is being let out of the U.S. economy in financial news. While there isn’t anything released this week that is going to meaningfully move the needle on the timing of the Fed’s decision, it was encouraging to see that the current restrictive policy stance is cooling the economy. That said, there is still enough strength underlying the economy to keep the Fed’s policy rate right where it is until later this year.

First up was the refresh of the first quarter’s GDP data. Top-line economic growth was shaved down a smidge, to a below trend 1.3% quarter-on-quarter (q/q, annualized) change. Consumer spending too was marked down, from 2.5% to a more trend-like 2.0%. That said, faced with persistently strong price growth and high interest rates, the ability of households to keep buying stuff and spending money on experiences has defied expectations. Specifically, the shift back to services spending has kept demand up on the primarily domestic portion of the economy facing a tight labor market. Moreover, there is room for this trend to run if households continue to adjust their expenditures back towards a pre-pandemic mix, where household services consumption accounted for just shy of 66% of personal consumer expenditures (compared to 64.6% as of April, Chart 1).

So, it came as a welcome surprise that April’s Personal Consumption and Expenditures (PCE) survey showed real PCE pull back 0.1% month-on-month (m/m). More good news came as the core PCE deflator edged down to 0.2% m/m, leaving the annual pace of price growth to 2.8%. That said, the three- and six-month core PCE inflation rates are still 3.5% and 3.2% (annualized), respectively, as the past few months of strong price growth continue to be felt.

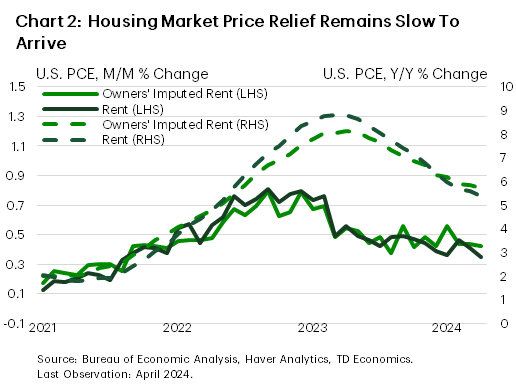

Importantly, while the deceleration in core price growth was welcome, special attention has to be paid to rents and housing costs that have been propping up core price growth. Together the two categories make up roughly 15% of PCE and will be critical to taming inflation. On this front, there was only marginal relief in April. Rent inflation came in at a “soft” 0.4% m/m (the print was 0.35% m/m unrounded). This is in line with the average reading from the prior five months (Chart 2). On the homeownership side too, implied rents came in at the same 0.4% m/m, roughly unchanged from the last few months. Sustained over a year, the 0.4% monthly pace would translate to 4.9% annual growth. The annual rates on the two shelter components are now cruising along at 5.7% and 5.4% for the imputed and actual rent measures, respectively.

For the Fed, April’s data were a step in the right direction, but there is still more work to be done before rate cuts become imminent. So now, all eyes are focused on data coming next week, and specifically the May payrolls report. After April’s real spending and payrolls data surprised to the downside, the focus will be for any signs that the month was not a one-off and weaker momentum continued into May.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.