Financial News Highlights

-

- In a widely expected move, the Federal Reserve held the policy rate steady in the target range of 5.25%-5.5% in major financial news.

- FOMC participants now expect fewer rate cuts this year, with the median projection showing just one cut by year-end (previously three).

- Consumer Price Index (CPI) inflation came in weaker than expected in May, with the core measure recording its softest monthly gain since August 2021.

The Data Will Light the Way

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

In a widely expected move, the Federal Reserve kept its policy rate unchanged holding the target range at 5.25%-5.5% for the seventh consecutive meeting. Accompanying the announcement, the FOMC also released a revised Summary of Economic Projects (SEP). In terms of the macroeconomic forecasts, there were few changes made relative to March in financial news. Expectations for growth this year and next remained unchanged at 2.1% and 2.0%, respectively, while the unemployment rate saw a modest upward revision of 0.1 percentage points in 2025 (to 4.2%) and 2026 (to 4.1%). The inflation forecast was nudged higher, with core PCE now expected to hold steady at 2.8% (previously 2.6%) through year-end, before slipping to 2.3% (previously 2.2%) by the end of the next year.

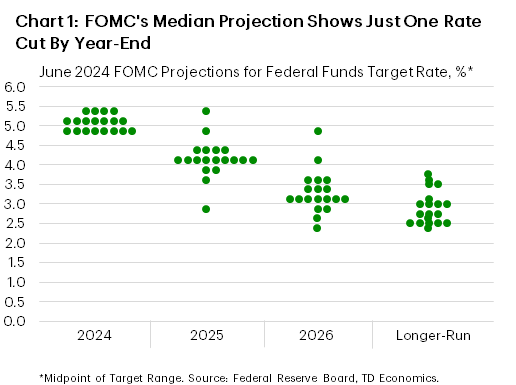

The most notable change in the SEP came from the Committee’s view on the future expectations of the policy rate. On the surface, the updated median Fed funds rate projection appears considerably more hawkish – now showing just one cut for this year as opposed to the three penciled in back in March. But a closer look at the dispersion of forecasts shows that FOMC members are nearly split between one (seven participants) and two (eight participants) cuts by year-end (Chart 1). Four members expect to keep the policy rate unchanged until next year.Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).During the press conference, Chair Powell acknowledged the last two softer-than-expected readings on inflation. However, he also reiterated that inflation “remains far too high” and that the FOMC needs to “greater confidence” before easing monetary policy. Whether that can be achieved over the next few months remains to be seen. As Powell noted in the press conference, “the data will light the way”.

Thomas Feltmate, Director & Senior Economist | 416- 944-5730

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

How quickly things can change! It was just six months ago that financial markets were positioned for six rate cuts by the end of this year. At the time, 50 basis points (bps) of cuts were expected to have happened by the June FOMC meeting. Well, that meeting has come and gone, and things haven’t quite shaped up as expected. The median forecast of FOMC participants is now showing just one rate cut by the end of this year. Bond traders are a bit more optimistic, currently pricing for two cuts, after a very soft CPI reading this week. A faster cooling in inflationary pressures helped to catapult the S&P 500 higher by over 1% on the week, while the 10-year Treasury dipped by 22 bps landing at 4.21%.

Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).

Broadly speaking, the upward revision to the ‘dots’ is a direct result of inflation having firmed through the first three-months of the year. However, the April inflation data showed some reprieve on that front, and this week’s May reading on CPI came in considerably below expectations. Core inflation rose by just 0.16% month-on-month – it’s softest monthly print since August 2021. The underlying details of the report were also constructive, with services inflation showing a notable cooling – entirely driven by the ‘supercore’ component – while goods prices were flat on the month. Encouragingly, the three-month annualized rate of change on core CPI slipped to 3.3% – a pace of price growth more consistent with late-2023 (Chart 2).This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.