Financial News Highlights

- The July report for the Consumer Price Index showed headline inflation fell below 3% for the first time since March 2021 in financial news.

- U.S. retail sales surpassed expectations in July, rising 1.0% month-on-month.

- Federal Reserve Chair Jerome Powell’s remarks during next week’s Jackson Hole Symposium will headline the week.

Inching Towards a Pivot

A relative state of calm presided over financial markets this week as incoming economic data continued to support the case for the first Federal Reserve rate cut in September in financial news. Inflation data for July showed that the annual change in prices fell below 3% for the first time since March 2021, while retail sales for the month came in above expectations. In response, equity markets rose on the week with the S&P 500 up 3.7% as of the time of writing, while U.S. Treasury yields steadied with the two-year yield roughly unchanged at 4.08%.

A relative state of calm presided over financial markets this week as incoming economic data continued to support the case for the first Federal Reserve rate cut in September in financial news. Inflation data for July showed that the annual change in prices fell below 3% for the first time since March 2021, while retail sales for the month came in above expectations. In response, equity markets rose on the week with the S&P 500 up 3.7% as of the time of writing, while U.S. Treasury yields steadied with the two-year yield roughly unchanged at 4.08%.

The Consumer Price Index (CPI) report for July showed that inflation picked up slightly relative to June in monthly terms, primarily driven by an uptick in shelter costs. However, the monthly increase in headline and core inflation was still below the level consistent with the Federal Reserve’s 2% target. As a result, the 3-month annualized percentage change in core CPI fell to its lowest level since early 2021 (Chart 1). While the Fed’s preferred inflation metric, core PCE, sat at 2.6% in June, momentum in CPI inflation continues to indicate that inflation pressures will likely ease further moving forward.

This was also evidenced by the Producer Price Index (PPI) report released this week, which showed that upstream production costs decelerated in July. Annual growth in producer prices had been rising through the first half of the year, which contributed to the slowing in the disinflation progress as these costs were likely passed on to consumers. Therefore, the reversal in this trend in July, especially if sustained, would likely provide further relief to consumer price growth moving forward. Taken together the trends in the July reports for PPI and CPI inflation support the case for the Federal Reserve to begin to gradually reduce interest rates at their next meeting in September.

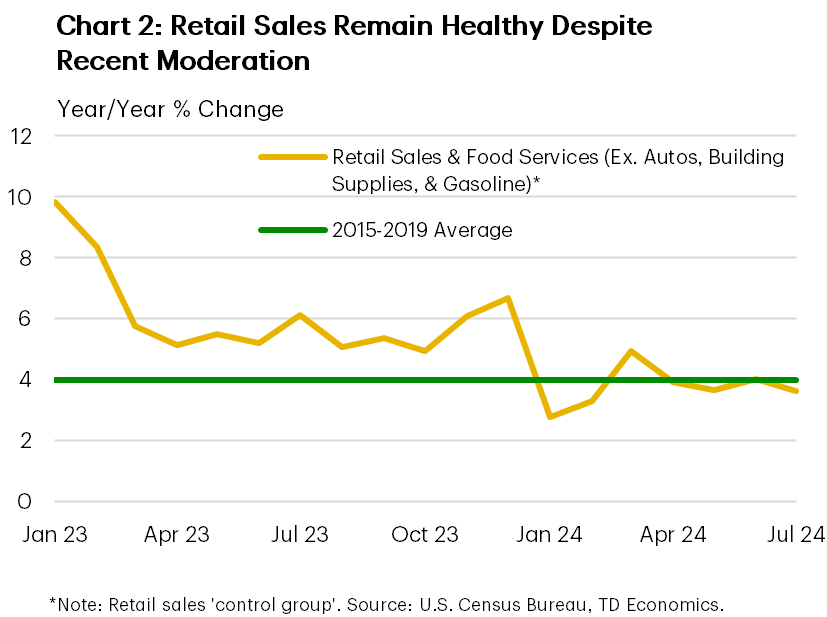

Fortunately, the moderation in price growth seen recently has not required a decline in consumer demand. As indicated by July retail sales, spending rose more than expected to start the second half of the year. This was in part driven by a rebound in auto sales after a cyber-attack against a dealership software firm depressed sales in June. Still, sales in the ‘control group’, which excludes the more volatile spending categories, remained healthy in July (Chart 2). The economy has exited a period of exceptionally strong demand and maintained stable momentum, but the Federal Reserve will be cognizant of the balance of risks moving forward.

Fortunately, the moderation in price growth seen recently has not required a decline in consumer demand. As indicated by July retail sales, spending rose more than expected to start the second half of the year. This was in part driven by a rebound in auto sales after a cyber-attack against a dealership software firm depressed sales in June. Still, sales in the ‘control group’, which excludes the more volatile spending categories, remained healthy in July (Chart 2). The economy has exited a period of exceptionally strong demand and maintained stable momentum, but the Federal Reserve will be cognizant of the balance of risks moving forward.

In the leadup to the Federal Reserve’s annual Jackson Hole Symposium next week, the slate of Fed speakers was relatively light this week. Governor Bowman, who is the only voting member of the FOMC who spoke this week, noted that upside risks to inflation remain and that caution would be warranted in considering future policy adjustments. Fed Presidents Bostic (Atlanta) and Musalem (St. Louis) broadly echoed these concerns, although both noted that interest rates would likely be lower in the second half of the year. Financial markets pared back their expectations for an outsized 50 basis-point (bps) cut in September this week, converging closer to our expectation for a 25bps cut, while they await further guidance from Chair Powell’s remarks scheduled for next Friday.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.