Financial News Highlights

- Minutes from the July 30-31 FOMC meeting as well as Chair Powell’s speech at Jackson Hole showed a clear commitment that the FOMC will start cutting rates in September in financial news.

- The Fed is likely to start slow, cutting by 25 basis points next month. But any signs of a more abrupt cooling in the labor market will result in a more aggressive pace of rate cuts.

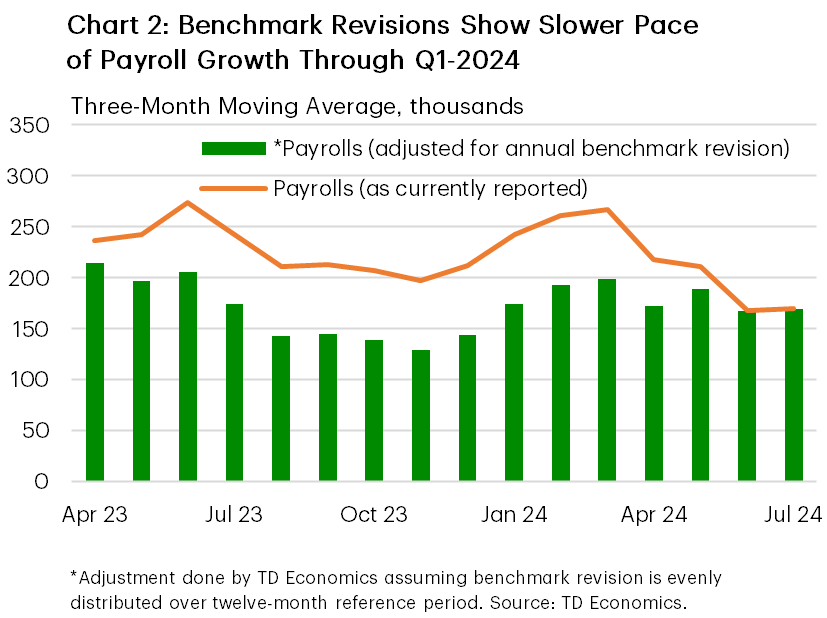

- Adding to evidence of a cooler labor market, annual benchmark revisions showed non-farm employment ended Q1 with less momentum than previously thought.

Fed Chair Powell Endorses September Rate Cut

It was a quiet week on the economic data calendar, but there was plenty of Fed communication for market participants to digest. The headliner was Fed Chair Powell’s speech at the annual Jackson Hole Symposium, where the Chairman signaled a clear desire for the FOMC to begin reducing its policy rate at its next meeting in September. The news hardly came as a surprise, particularly coming after the release of the July 30-31 FOMC minutes, which indicated that the “vast majority of participants” supported cutting rates at the next meeting. Though equity markets see-sawed through most of the week, a clear commitment from Powell that the Fed will soon start loosening its policy stance helped to fuel a late-week rally, with the S&P 500 looking to end the week up 1.3%. Bond yields across the curve were lower by 10-15 basis-points (bps) on the week, with the 10-year Treasury sitting at 3.8% at the time of writing.

It was a quiet week on the economic data calendar, but there was plenty of Fed communication for market participants to digest. The headliner was Fed Chair Powell’s speech at the annual Jackson Hole Symposium, where the Chairman signaled a clear desire for the FOMC to begin reducing its policy rate at its next meeting in September. The news hardly came as a surprise, particularly coming after the release of the July 30-31 FOMC minutes, which indicated that the “vast majority of participants” supported cutting rates at the next meeting. Though equity markets see-sawed through most of the week, a clear commitment from Powell that the Fed will soon start loosening its policy stance helped to fuel a late-week rally, with the S&P 500 looking to end the week up 1.3%. Bond yields across the curve were lower by 10-15 basis-points (bps) on the week, with the 10-year Treasury sitting at 3.8% at the time of writing.

Two years ago, Chair Powell delivered a very somber message during his speech at Jackson Hole, stating the Federal Reserve will do “whatever it takes to restore price stability” even if that meant “inflicting some economic pain” in financial news. At the time, inflation was sitting at a multi-decade high while the labor market had tightened to a degree not seen in recent history. It had become obvious that policymakers had fallen well behind the curve and were scrambling to play catch-up. While many feared that the FOMC’s swift actions of quickly raising the policy rate (Chart 1) risked overtightening and potentially tipping the economy into a recession, the downturn never materialized.

During his speech Friday morning, Chair Powell acknowledged the progress the Fed has made over the past two years, specifically noting that the upside risks to inflation have diminished while the downside risks to employment have increased. While Powell offered nothing in terms of the speed of adjustment, other policymakers speaking this week highlighted the importance of a “gradual” and “methodical” approach to loosening policy, which supports a 25 basis point cut in September. However, Powell also emphasized that the FOMC “does not seek or welcome any further cooling in the labor market”, which suggests the next several employment reports will be critical in determining the future path of the policy rate.

During his speech Friday morning, Chair Powell acknowledged the progress the Fed has made over the past two years, specifically noting that the upside risks to inflation have diminished while the downside risks to employment have increased. While Powell offered nothing in terms of the speed of adjustment, other policymakers speaking this week highlighted the importance of a “gradual” and “methodical” approach to loosening policy, which supports a 25 basis point cut in September. However, Powell also emphasized that the FOMC “does not seek or welcome any further cooling in the labor market”, which suggests the next several employment reports will be critical in determining the future path of the policy rate.

Fears of a further cooling in the labor market aren’t completely unfounded. Earlier this week, the BLS released its preliminary annual benchmark revisions for non-farm employment, which showed that payrolls were 818 thousand less over the twelve-month period ending in March 2024 – the largest downward adjustment since 2009. This implies that job gains likely averaged closer to 174 thousand per-month over the reference period, as opposed to the 242 thousand currently reported (Chart 2).

Even after incorporating the revisions, there’s nothing yet to suggest that the labor market has overcorrected. This is why we feel that the FOMC is likely to opt for a more gradual approach in the beginning. However, it is clear that policymakers have become hypervigilant of the labor market and any further signs of cooling is likely to bring a more aggressive path for rate cuts.

Thomas Feltmate Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.