Financial News Highlights

- The second estimate of Q2 GDP revealed that the U.S. economy grew at 3.0% annualized, a bit stronger than previously reported, thanks to an upward revision in consumer spending in financial news.

- Spending momentum continued into July, outstripping income growth for the sixth consecutive month and pushing the savings rate to a two-year low of 2.9%.

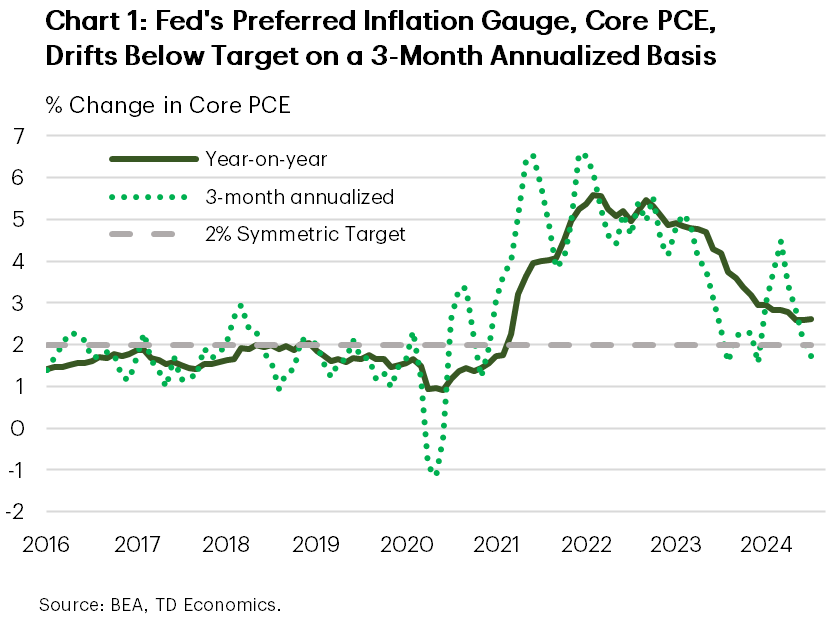

- Core PCE inflation held steady at 2.6% year-on-year in July, while the three-month annualized rate of change fell below the Fed’s 2% inflation target.

Fed to Tilt Focus to Labor Market as it Tees Up First Rate Cut

The Labor Day weekend is upon us, providing an opportunity to celebrate the achievements of the American worker. Keeping with the labor market theme, now that the Fed appears relatively confident that inflation will return to target, we believe it will put a little more emphasis the other side of its dual mandate – the goal of maximum employment – to determine the speed and size of policy easing. In that vein, next week’s payrolls report can’t come soon enough. This week’s data, meanwhile, did little to rock the boat, coming in broadly positive. Amidst this backdrop, long-term yields trended modestly higher, while the S&P 500 looks to end the week lower by 0.6% as of the time of writing.

The Labor Day weekend is upon us, providing an opportunity to celebrate the achievements of the American worker. Keeping with the labor market theme, now that the Fed appears relatively confident that inflation will return to target, we believe it will put a little more emphasis the other side of its dual mandate – the goal of maximum employment – to determine the speed and size of policy easing. In that vein, next week’s payrolls report can’t come soon enough. This week’s data, meanwhile, did little to rock the boat, coming in broadly positive. Amidst this backdrop, long-term yields trended modestly higher, while the S&P 500 looks to end the week lower by 0.6% as of the time of writing.

A second read on U.S. GDP revealed an even better growth profile of 3.0% annualized in the second quarter (vs. 2.8% previously), thanks in large part to an upward revision in consumer spending (2.9% vs. 2.3% previously). But this week’s highlight was the July personal income and spending (PCE) report. The latter showed that overall and core PCE inflation held steady on an annual basis, coming in at respectively 2.5% and 2.6% in July. Looking to more recent trends, on a 3-month annualized basis, core PCE eased to 1.7% in July from 2.1% in the month prior, suggesting we’re likely to see more cooling in inflationary pressures in the months ahead (Chart 1).

The PCE report also shed light on consumer spending, which had a relatively healthy start to the third quarter in financial news. Real spending rose by 0.4% month-over-month (m/m) in July – an acceleration from 0.3% in the month prior, with both goods and service spending chipping in with healthy gains. However, real disposable personal income continued to trail behind (+0.1%), which meant consumers had to dip into their savings to sustain the higher rate of spending. As a result, the personal savings rate fell to a two-year low of 2.9%.

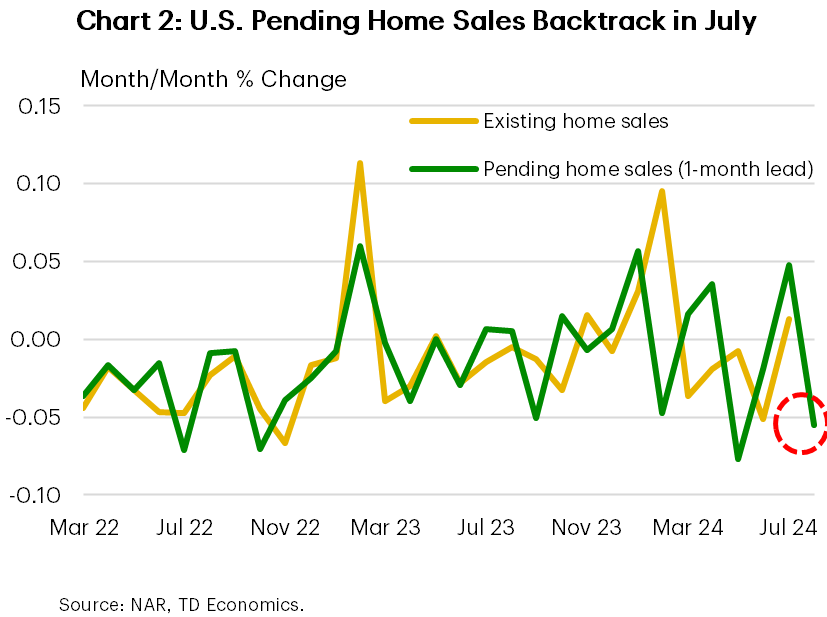

Other consumer-related indicators continued to paint a nuanced picture. Americans were a little more upbeat in August, with the Conference Board confidence measure rising to a six-month high, thanks in large part to an improvement in the “expectations” subcomponent. Still, plans to buy large ticket items, including cars, homes, and major appliances, all trended lower on the month. And it’s not just survey data showing a consumer’s reluctance to make big purchases. Pending home sales – a leading indicator for existing home sales – fell sharply in July (-5.5%), driving home the point that the recent pullback in interest rates has so far failed to spark a sustained improvement in sales (Chart 2).

Other consumer-related indicators continued to paint a nuanced picture. Americans were a little more upbeat in August, with the Conference Board confidence measure rising to a six-month high, thanks in large part to an improvement in the “expectations” subcomponent. Still, plans to buy large ticket items, including cars, homes, and major appliances, all trended lower on the month. And it’s not just survey data showing a consumer’s reluctance to make big purchases. Pending home sales – a leading indicator for existing home sales – fell sharply in July (-5.5%), driving home the point that the recent pullback in interest rates has so far failed to spark a sustained improvement in sales (Chart 2).

Next week, attention will turn towards the August payrolls report, which will help shape whether the Fed cuts by 25 or 50 basis points at its next rate decision in September. Market expectations call for some rebound in job gains relative to July’s gain of 114,000. The recent steadying of both jobless claims and job postings suggests that the chances of another downside miss is less likely, which favors a 25 basis point cut in September.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.