Financial News Highlights

- Markets have been weighing the prospect that the Federal Reserve will opt for a 0.5 percentage point cut in the federal funds rate next week in financial news.

- Core consumer price index inflation surprised to the upside, lifted by a strong print from owners’ equivalent rent.

- The breadth of inflation continues to gradually narrow, but a still resilient economy supports the case for a standard 0.25 point cut at next week’s Fed meeting.

Here Comes the Cut

After Vice President Harris and former President Trump took their turn in the spotlight on Tuesday night, focus turned back to inflation and where the Federal Reserve is likely to take interest rates from here. Markets were weighing the possibility that the deteriorating economic backdrop was opening the door to a 50 basis-point cut in the Fed Funds rate next week. Alas, inflation didn’t seem to want to cooperate, as Consumer Price Index (CPI) inflation clocked in at 2.5%, as expected, with the core measure surprising to the upside amid an upturn in shelter prices. Current market pricing puts the odds of a 50 basis-point cut at basically a coin toss, but we think the state of the economy and the details of the report argue for a smaller 25 basis-point move next week.

After Vice President Harris and former President Trump took their turn in the spotlight on Tuesday night, focus turned back to inflation and where the Federal Reserve is likely to take interest rates from here. Markets were weighing the possibility that the deteriorating economic backdrop was opening the door to a 50 basis-point cut in the Fed Funds rate next week. Alas, inflation didn’t seem to want to cooperate, as Consumer Price Index (CPI) inflation clocked in at 2.5%, as expected, with the core measure surprising to the upside amid an upturn in shelter prices. Current market pricing puts the odds of a 50 basis-point cut at basically a coin toss, but we think the state of the economy and the details of the report argue for a smaller 25 basis-point move next week.

First, and foremost, this week’s report is a minor setback and not a return to the widespread inflation we saw in 2022. Most of the gain was powered by a strong showing in shelter costs, specifically owners’ equivalent rent (Chart 1). Growth here ticked up for the month, but this has been a steady contributor to inflation this cycle. While the rate could moderate slightly heading into the fall, it was the strongest print in seven months in financial news. Now, importantly, the Fed’s preferred measure looks at core personal consumption expenditure (PCE) inflation, where shelter prices carry a smaller weight. So, this upturn will have a comparably smaller impact on the Fed’s preferred inflation measure.

As for the two other major inflationary culprits, airfares and vehicle insurance, there is reason to expect moderation. New and used vehicle prices have cooled substantially, and after rising car valuations drove insurance rates higher, this impulse should continue to fade. On airfares, last month broke a string of negative prints for the category – an element of giveback that could easily fade.

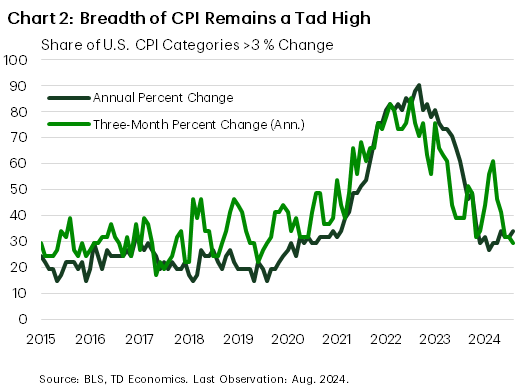

All of which is to say, consumer price inflation is gradually becoming confined to fewer categories (Chart 2). Taking a lens to the three-month percent change of the CPI categories, the share of categories with prices still rising above a three percent (annualized) rate has been below the pre-pandemic average for the past three months. After the uptick in inflation last spring, the return to a downward trajectory is welcome. This trend will need to continue for few more months still before the year-on-year prints start to show the same normalization, but things are pointing in the right direction.

All of which is to say, consumer price inflation is gradually becoming confined to fewer categories (Chart 2). Taking a lens to the three-month percent change of the CPI categories, the share of categories with prices still rising above a three percent (annualized) rate has been below the pre-pandemic average for the past three months. After the uptick in inflation last spring, the return to a downward trajectory is welcome. This trend will need to continue for few more months still before the year-on-year prints start to show the same normalization, but things are pointing in the right direction.

The data suggest that the Fed’s policy rate does not need to be as restrictive as it is, but while former NY Fed President Dudley this week suggested there was “a strong case” for a 50 basis- point cut, we think this is a tad premature. Between this week’s CPI report showing unexpected strength in core consumer prices, the upside surprise in the producer price index, and a labor market that continues to steadily add jobs, there is enough strength to suggest aggressively easing monetary policy is not yet warranted. Our view remains that a 25 basis-point cut next week is the most likely outcome, with two more cuts coming by year-end.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.