Financial News Highlights

- The Federal Reserve’s preferred inflation metric, the core PCE index, continued to cool in August with the 3- and 6-month annualized trends converging closer to the Fed’s 2% target in financial news.

- Federal Reserve officials who spoke this week noted that the slowing labor market was a key consideration in their monetary policy decision last week and that further rate cuts were expected moving forward.

- Congress managed to pass a continuing resolution this week to fund the federal government through December 20th, removing the risk of a government shutdown until after the upcoming election.

Government Shutdown Averted as Price Pressures Continue to Ease

The first week of fall was largely consumed by lingering consternation regarding the Federal Reserve’s latest monetary policy decision. Federal Reserve officials who spoke this week provided further clarity on the central bank’s rationale to go big with the first rate cut in over four years, as the latest reading on inflation showed price pressures continued to cool in August. Financial markets were little changed on the week, with Treasury yields rising a few basis-points and the S&P 500 up 1.0% as of the time of writing.

The first week of fall was largely consumed by lingering consternation regarding the Federal Reserve’s latest monetary policy decision. Federal Reserve officials who spoke this week provided further clarity on the central bank’s rationale to go big with the first rate cut in over four years, as the latest reading on inflation showed price pressures continued to cool in August. Financial markets were little changed on the week, with Treasury yields rising a few basis-points and the S&P 500 up 1.0% as of the time of writing.

Friday’s personal income & spending data release for August showed that the health of the American consumer remained favorable on aggregate through the end of the summer. Real personal consumption expenditures rose 0.1% relative to July, with goods spending roughly flat while service expenditures expanded. Consumers continued to receive support from healthy real disposable personal income gains (+3.1% year-on-year in August), although this growth has continued to moderate. This has led to some slowing in consumer spending, which has helped to push the three- and six-month annualized percentage change in core PCE inflation closer to the Fed’s 2% target after the flare-up earlier in the year (Chart 1).

With inflation pressures continuing to cool, the Federal Reserve’s downward policy path trajectory appears to continue to be supported by the incoming data. Federal Reserve officials who spoke this week broadly echoed the statements of Chair Powell last week, noting that the balance of risks has shifted towards the labor market and that ensuring a soft landing would merit looser financial conditions moving forward. Although the majority of officials who spoke this week were focused on downside risks to the economy, Governor Bowman, the lone dissenting vote from last week’s decision, noted that inflation risks remained elevated and that this would necessitate caution moving forward. Market pricing is roughly 50/50 between a quarter- and a half-point cut at the next meeting in November as of the time of writing.

Markets will likely be equally focused on fiscal policy risks moving forward with the U.S. election now less than six weeks away. Thankfully, Congress managed to avoid the risk of a government shutdown this week by passing a continuing resolution through to December 20th. However, with federal government funding and the debt limit suspension both now expiring at the end of the year, fiscal risks are likely to remain top-of-mind in the final two months of the year.

Markets will likely be equally focused on fiscal policy risks moving forward with the U.S. election now less than six weeks away. Thankfully, Congress managed to avoid the risk of a government shutdown this week by passing a continuing resolution through to December 20th. However, with federal government funding and the debt limit suspension both now expiring at the end of the year, fiscal risks are likely to remain top-of-mind in the final two months of the year.

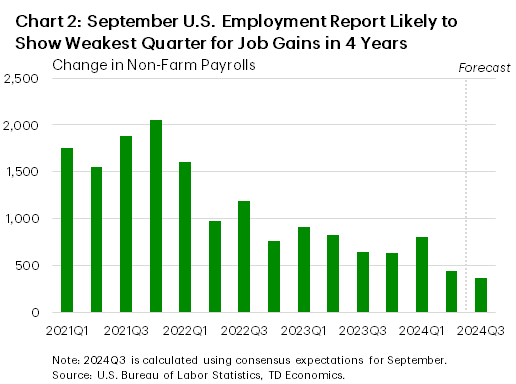

Looking ahead to next week, the biggest item on the docket will be the September employment report released on Friday, with consensus expectations for a gain of 130k jobs. This will likely cap-off the weakest quarter for job gains since the onset of the pandemic (Chart 2). Markets will also be watching Chair Powell’s speech at the National Association for Business Economics Annual Meeting on Monday, in addition to the Vice-Presidential debate in New York City on Tuesday.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.