Financial News Highlights

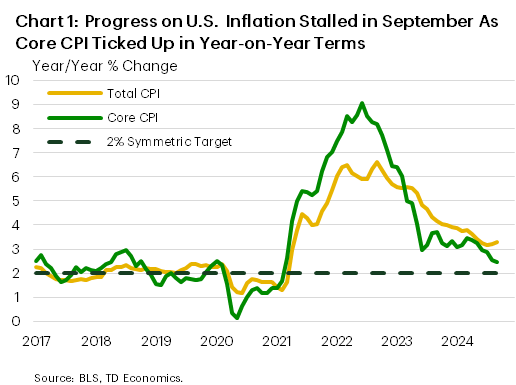

- Progress on the inflation front appears to have stalled at the end of the third quarter in financial news, as core CPI inflation ticked up, albeit modestly, by 0.1 percentage point to 3.3% year-on-year in September.

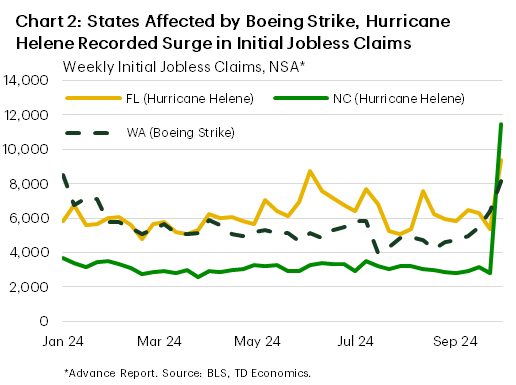

- Initial jobless claims surged higher by last week, as states affected by Hurricane Helene (FL, NC) and the ongoing Boeing strike (WA) recorded outsized increases to their unadjusted initial jobless claims.

- Between stronger job growth, and slower progress on inflation, we expect the Fed to cut rates more gradually, with two quarter-point cuts in November and December.

Rates to Fall, But Not So Fast

The second week of October continued to reflect the theme that began at last week’s close in financial news. A stronger-than-expected payrolls report last Friday drove home the point that the U.S. labor market is holding up better than previously thought, while this week’s CPI report showed progress on the inflation front stalling. All of this suggests that the Fed is likely to slow the pace of rate cuts next month. Bond yields continued the climb higher this week, with the 10-Year yield up another 10 basis points, closing out the week at 4.1%. Equity markets managed to eke out a decent gain, with the S&P 500 up roughly 1% from last week’s close, as of the time of writing.

The second week of October continued to reflect the theme that began at last week’s close in financial news. A stronger-than-expected payrolls report last Friday drove home the point that the U.S. labor market is holding up better than previously thought, while this week’s CPI report showed progress on the inflation front stalling. All of this suggests that the Fed is likely to slow the pace of rate cuts next month. Bond yields continued the climb higher this week, with the 10-Year yield up another 10 basis points, closing out the week at 4.1%. Equity markets managed to eke out a decent gain, with the S&P 500 up roughly 1% from last week’s close, as of the time of writing.

Total inflation as measured by CPI cooled in September, easing from 2.5% year-on-year (y/y) to 2.4%, largely due to falling energy prices. However, the good news ended there. Core CPI inflation rose a tenth of a percentage point, more than the consensus forecast, which pushed the twelve-month change higher to 3.3% y/y (Chart 1). Price growth in the important ‘shelter’ category eased, though we saw broader price pressures heat up across most other service categories, while core goods prices added to overall inflationary pressure – a first in seven months.

With progress on the inflation front stalling and the labor market holding up well, futures markets are now pricing just an 80% probability that the Fed will cut by 25-basis points next month. Minutes from the last FOMC meeting show that the Fed’s strong start to the easing cycle in September was thought of as a “recalibration” to help bring restrictive monetary policy into “better alignment” with recent indicators of inflation and the labor market, and that this should not be interpreted as the new pace of policy easing over the coming months. We anticipate the Fed will deliver two additional 25 basis point cuts by the end of this year.

However, it’s important to note that the Fed will remain heavily data dependent in setting monetary policy. This will become increasingly difficult over the coming months, with large distortions likely to be seen in October/November data because of Hurricane’s Helene and Milton and the ongoing Boeing strike. Besides the tragic loss of life, the recent hurricanes have left behind a path of destruction in the Southeast, which will exude some near-term weakness.

However, it’s important to note that the Fed will remain heavily data dependent in setting monetary policy. This will become increasingly difficult over the coming months, with large distortions likely to be seen in October/November data because of Hurricane’s Helene and Milton and the ongoing Boeing strike. Besides the tragic loss of life, the recent hurricanes have left behind a path of destruction in the Southeast, which will exude some near-term weakness.

The impacts of Boeing and Helene appear to already be featuring in employment data, with a sharp jump in initial jobless claims (up 33,000 to a seasonally adjusted 258,000 last week) tied in part to these events. Large increases in initial jobless claims were recorded in affected states such as Florida and North Carolina (Helene) and Washington (Boeing) (see Chart 2). We anticipate the Fed will look past the transient nature of some of these impacts as it continues to ease monetary policy next month, but communication as related to the next cut will require considerable effort given the many factors at play.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.