Financial News Highlights

- The retail sales report once again reinforced the message that the U.S. consumer continues to brush off headwinds in financial news.

- Personal income growth, some remaining pandemic savings, and a healthy labor market should help to support trend-like growth in personal consumption expenditures into early 2025.

- A still healthy labor market, and a commitment to data dependency means a measured and deliberate approach to interest rate reductions.

Slow and Steady

U.S. Treasury yields were on the rise again this week (Chart 1) as a brighter picture of the consumer pared back rate cut bets in financial news. The September retail sales report once again reinforced the message that the consumer continues to plow ahead, brushing off headwinds from higher rates and two years’ worth of rapid cost-of-living increases. Policymakers and markets continue to assess that interest rates need to fall further, but the timing and level of where they ultimately land remains hotly debated.

U.S. Treasury yields were on the rise again this week (Chart 1) as a brighter picture of the consumer pared back rate cut bets in financial news. The September retail sales report once again reinforced the message that the consumer continues to plow ahead, brushing off headwinds from higher rates and two years’ worth of rapid cost-of-living increases. Policymakers and markets continue to assess that interest rates need to fall further, but the timing and level of where they ultimately land remains hotly debated.

Data are streaming in and showing consumers, the backbone of the U.S. economy, are willing and able to spend on goods and services at a healthy pace. Retail sales figures for September rose 0.4% month-on-month, beating out economists’ expectations. Moreover, the “control group” of less volatile expenditure categories surged 0.7% for the month as spending on clothing, personal care and miscellaneous goods surged. With stronger than expected economic news, bond yields surged, rising 6 basis points (bps) through Thursday’s close.

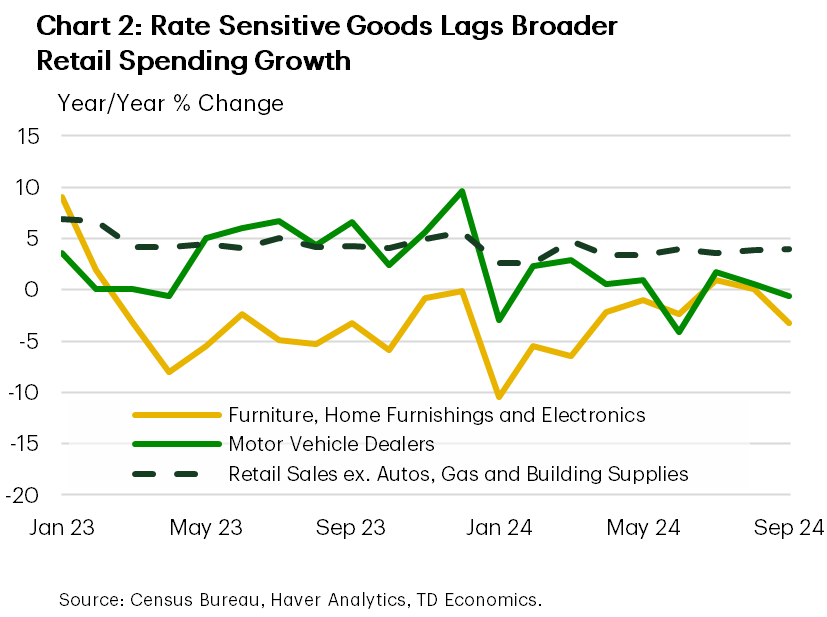

The print suggests plenty of momentum in consumption expenditures into the third quarter, providing a fillip to GDP growth. However, strong doesn’t mean that monetary policy isn’t exerting pressure on households. Sales of motor vehicle dealers were down marginally, as were expenditures on furniture and electronics stores (Chart 2). These categories of goods are more interest rate sensitive, leaving them most susceptible to the still elevated interest rate environment.

However, as we noted this week, the recent upward revision to personal income means households are still holding excess savings that can be deployed. While the funds are mostly concentrated among higher income households that are less likely to spend, their availability means that demand for durable goods could rise as interest rates slowly fall. This sentiment was echoed by Fed Governor Waller this week, when he noted that his “business contacts believe that there is considerable pent-up demand for durable goods, home improvements and other big-ticket items”.

However, as we noted this week, the recent upward revision to personal income means households are still holding excess savings that can be deployed. While the funds are mostly concentrated among higher income households that are less likely to spend, their availability means that demand for durable goods could rise as interest rates slowly fall. This sentiment was echoed by Fed Governor Waller this week, when he noted that his “business contacts believe that there is considerable pent-up demand for durable goods, home improvements and other big-ticket items”.

While the labor market is gradually rebalancing, personal income growth is still robust and some remaining pandemic savings should help to support trend-like growth in personal consumption expenditures into early 2025. Carefully balancing strong growth and a healthy labor market against the risks of a flare-up in inflation will likely leave the Fed adopting a relatively cautious and data dependent approach to interest rates – caution Governor Waller reiterated stating, “monetary policy should proceed with more caution on the pace of rate cuts than was needed at the September meeting.”

Policy remains highly restrictive, and more easing is on the way. A still healthy labor market, and a commitment to data dependency means a measured and deliberate approach to policy. This leaves us thinking the Fed will deliver two more quarter point cuts through 2024.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.