Financial News Highlights

- U.S. Treasury yields continued to rise as the race for the White House tightened, leading to elevated uncertainty regarding the future path of fiscal policy in financial news.

- Federal Reserve speakers this week noted that further reductions in interest rates would be warranted, although incoming data supported a cautious approach.

- Existing home sales fell to a fourteen year low in September. Elevated interest rates, combined with expectations for lower rates moving forward, worked to keep demand subdued.

Countdown to Election Day

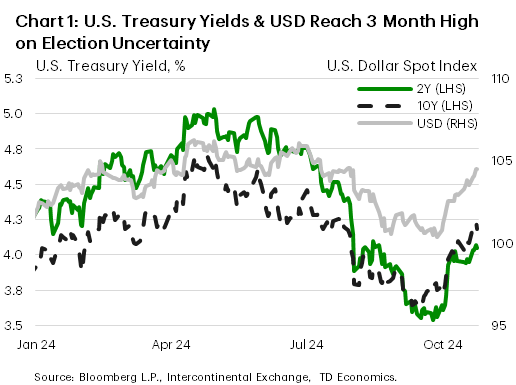

One of the most anticipated global events of 2024 is now nearly a week away. As financial markets anxiously await the outcome of the U.S. presidential and congressional elections, we have seen U.S. Treasury yields and the U.S. dollar rise to three-month highs (Chart 1). The uptick which began earlier this month was initially incited by stronger-than-expected economic data, but recent movements have also likely been driven by the narrowing in the polls for the U.S. presidential election. Given that the election will determine the path of fiscal policy moving forward, and by extension monetary policy, uncertainty related to the outcome is likely to remain a weight on financial markets through to November 5th.

One of the most anticipated global events of 2024 is now nearly a week away. As financial markets anxiously await the outcome of the U.S. presidential and congressional elections, we have seen U.S. Treasury yields and the U.S. dollar rise to three-month highs (Chart 1). The uptick which began earlier this month was initially incited by stronger-than-expected economic data, but recent movements have also likely been driven by the narrowing in the polls for the U.S. presidential election. Given that the election will determine the path of fiscal policy moving forward, and by extension monetary policy, uncertainty related to the outcome is likely to remain a weight on financial markets through to November 5th.

Elevated interest rates continued to dampen housing market activity in September, as existing home sales fell to their lowest level since 2010! Demand is also likely being restrained in part by consumer expectations for lower interest rates moving forward, with Federal Reserve Chair Powell indicating that rates would likely be trending lower through the coming year during his press conference last month. Existing home sales are likely to remain subdued in the near-term as mortgage rates moved back above 6½% in October. Nevertheless, the housing market is expected to thaw over the coming year as the Federal Reserve continues to reduce borrowing costs.

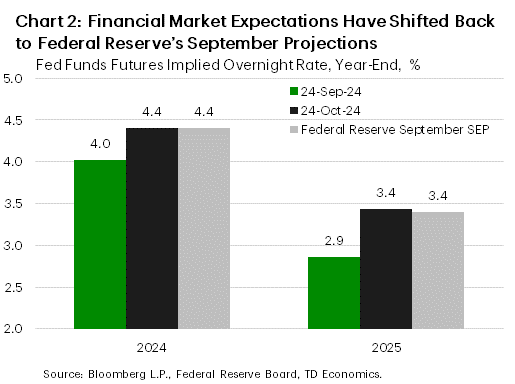

The Federal Reserve will be entering its pre-interest rate decision blackout period this weekend, with no further updates expected until Chair Powell’s post-meeting press conference on November 7th. The Fed officials we heard from this week stated that the strength of incoming economic data would warrant caution in future policy decisions, but all speakers noted that the trajectory of interest rates would continue to be downward. Market pricing has pulled back their expectations for rate cuts, but they are now realigned with the Federal Reserve’s median projection from the September Summary of Economic Projections (Chart 2).

The Federal Reserve will be entering its pre-interest rate decision blackout period this weekend, with no further updates expected until Chair Powell’s post-meeting press conference on November 7th. The Fed officials we heard from this week stated that the strength of incoming economic data would warrant caution in future policy decisions, but all speakers noted that the trajectory of interest rates would continue to be downward. Market pricing has pulled back their expectations for rate cuts, but they are now realigned with the Federal Reserve’s median projection from the September Summary of Economic Projections (Chart 2).

Next week sees a bumper crop of data releases that will be key inputs to the Federal Reserve’s next interest rate decision. The advance estimate for real GDP growth in the third quarter is expected to show the economy continuing to grow at a strong pace of 3.0%. While employment growth remained solid in the third quarter, October’s employment report due out next Friday is expected to show a deceleration in job gains (125k vs. 254k in September). The Federal Reserve will also be monitoring the release of their preferred inflation metric next week, core PCE, which is expected to show a modest decline to 2.6% in September.

Assuming there are no surprises in the incoming data, the Federal Reserve is expected to continue to cut rates at a pace of 25 basis points per meeting through the end of the year. Chair Powell’s remarks on November 7th will be monitored closely for guidance, although they may be competing with the results of the 2024 election for the attention of financial markets. Suffice it to say, markets will not be left wanting for important developments in the coming weeks.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.