Financial News Highlights

- The U.S. economy expanded by a robust 2.8% quarter-on-quarter (annualized) in the third quarter, only a touch slower than the 3% pace seen in Q2 in financial news.

- Growth in both income and consumer spending picked up in September while core PCE inflation held steady at 2.7% y/y.

- Employment was essentially flat in October, with the economy adding a meager 12k jobs – well below the already-low 100k consensus estimate. The ongoing Boeing strike and disruptions related to Hurricanes Helene and Milton both weighed on the headline.

The U.S. GDP data delivers treats, but the payrolls report plays tricks

Next week all eyes will be on the U.S. elections and the Federal Reserve meeting. However, this week the focus has been on the health of the U.S. economy – an important reference point for both presidential candidates and the Fed.

Next week all eyes will be on the U.S. elections and the Federal Reserve meeting. However, this week the focus has been on the health of the U.S. economy – an important reference point for both presidential candidates and the Fed.

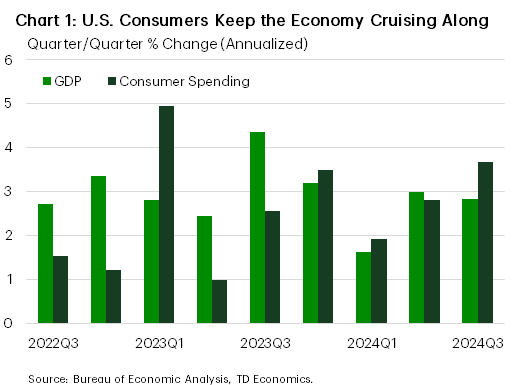

Wednesday’s advanced GDP report showed that the U.S. economy is alive and well. Coming on the heels of the solid 3% gain in Q2, the economy expanded by 2.8% (quarter-over-quarter annualized) in Q3. Consumers were the belle of the ball, with spending accelerating to 3.7%, or the fastest pace since Q1 2023 (Chart 1).

This ongoing resilience was further echoed in September’s personal income and spending report. It showed that spending increased by 0.5% m/m in September, outpacing income and indicating that consumers kept their purse strings open as Q3 wrapped up in financial news. Lower prices at the pump in recent weeks may have boosted confidence, giving consumers some reprieve from the ever-rising prices elsewhere. On that front, core PCE deflator – which excludes food and energy – rose 0.3% m/m in September. This held the twelve-month change steady at 2.7% for the third consecutive month, but this was largely due to “base effects”. Importantly, the 3-and-6-month annualized rates of change sit just above the Fed’s 2% inflation target, suggesting we’re likely to see more downward pressure on the year-ago measure in the months ahead.

As we noted in a recent report, there are several reasons consumers may have more momentum than previously anticipated, such as a notable upgrade to personal income in first half of 2024 and a larger buffer of savings. However, the savings cushion is quickly dwindling, with the personal saving rate having now declined for three consecutive months. This suggests we’re likely to see some moderation in consumer spending to something more consistent with a trend-like pace of around 2% in the months ahead.

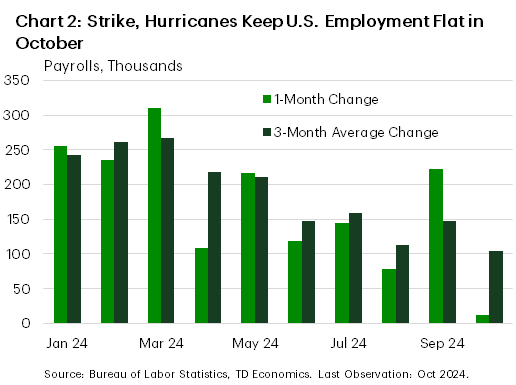

On that note, October’s payroll report was expected to be a weak one, but still surprised to the downside. The economy added just 12k jobs in October, well below the expectation for a 100k gain, while. Adding to the disappointment, downward revisions shaved 112k from the two prior months’ gains. The ongoing Boeing strike helped to cut over 40k from the headline number in October, while Hurricanes Helene and Milton also likely had a heavy hand weighing down the payrolls figure.

On that note, October’s payroll report was expected to be a weak one, but still surprised to the downside. The economy added just 12k jobs in October, well below the expectation for a 100k gain, while. Adding to the disappointment, downward revisions shaved 112k from the two prior months’ gains. The ongoing Boeing strike helped to cut over 40k from the headline number in October, while Hurricanes Helene and Milton also likely had a heavy hand weighing down the payrolls figure.

As a result, the Fed will likely look through October’s noisy employment data, and instead focus more on the broader trends showing that the labor market is decelerating but not necessarily deteriorating. Moreover, with the Fed’s preferred wage metric – the Employment Cost Index – showing wage pressures now growing at a pace roughly consistent with 2% inflation, the FOMC should have all the confidence they need to continue to gradually reduce the policy rate. We expect the Fed to cut by 25 basis-points at next week’s meeting. While this decision seems almost certain, the U.S. elections remain a wild card, promising to keep everyone on edge until the final votes are tallied.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.