Financial News Highlights

- Progress on the inflation front appears to have stalled in financial news. Core CPI inflation held steady in October, while the trend over the past three months has accelerated.

- October retail sales were also solid, putting consumer spending in the fourth quarter on a very solid footing.

- Chair Powell moved markets on Thursday by saying that the Fed may not be in a hurry to cut rates. This sent Treasury yields and the dollar moderately higher, while weighing on equities.

Inflation Progress Stalls, Fed in No Hurry to Cut Rates

Political developments continued to dominate the limelight this week. Republicans retained a slim majority in the House, cementing control over both chambers of Congress and the Presidency. In the meantime, President-elect Trump is hitting the ground running, announcing cabinet appointments and White House staff positions. The choices reinforce the campaign themes of slower immigration, along with a tougher stance on China and trade. Amidst the political noise, equity markets remained sanguine early in the week, but did lose considerable steam at the end of the week on growing signs that the Fed may not be in a rush to cut rates. Chief among these are signs of slowing progress on the inflation front.

Political developments continued to dominate the limelight this week. Republicans retained a slim majority in the House, cementing control over both chambers of Congress and the Presidency. In the meantime, President-elect Trump is hitting the ground running, announcing cabinet appointments and White House staff positions. The choices reinforce the campaign themes of slower immigration, along with a tougher stance on China and trade. Amidst the political noise, equity markets remained sanguine early in the week, but did lose considerable steam at the end of the week on growing signs that the Fed may not be in a rush to cut rates. Chief among these are signs of slowing progress on the inflation front.

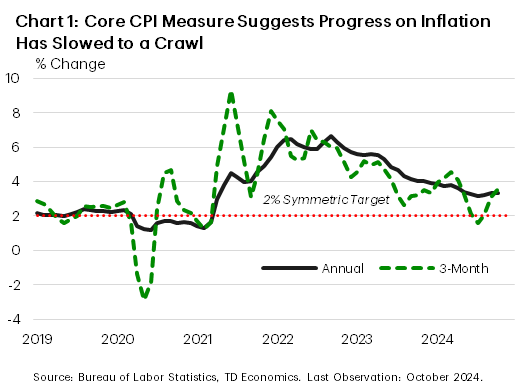

Headline inflation as tracked by the consumer price index (CPI) ticked up in October (see commentary). Inflation pressures were also a little hot under the collar in the core measure, which rose 0.3% m/m for the third consecutive month. Core inflation held steady at 3.3% on a year-on-year basis in October, but the trend over the past three months heated up (Chart 1). Services inflation is showing signs of stickiness, with price growth for core services holding at 4.8% y/y for the second month in a row. This suggests that after some fast initial progress, the final stage of getting inflation back down to the Fed’s 2% target may indeed be a long slog. Producer prices drove home the same point, with growth in core producer price inflation accelerating to 3.1% y/y in October from 2.9% in the month prior.

These latest inflationary trends are not what the Fed wants to see. At a speech this week, Fed Chair Powell noted that “the economy is not sending any signals that we need to be in a hurry to lower rates”, adding that “the strength we are currently seeing in the economy gives us the ability to approach our decisions carefully”. A relatively healthy October retail sales report released on Friday lends support to that latter point. Helped along by an outsized gain in autos, decent growth in retail sales in October built on a healthy September gain to provide a solid start for consumer spending in the fourth quarter, which looks to be tracking 3.3% annualized, up from a few ticks under 3% previously.

These latest inflationary trends are not what the Fed wants to see. At a speech this week, Fed Chair Powell noted that “the economy is not sending any signals that we need to be in a hurry to lower rates”, adding that “the strength we are currently seeing in the economy gives us the ability to approach our decisions carefully”. A relatively healthy October retail sales report released on Friday lends support to that latter point. Helped along by an outsized gain in autos, decent growth in retail sales in October built on a healthy September gain to provide a solid start for consumer spending in the fourth quarter, which looks to be tracking 3.3% annualized, up from a few ticks under 3% previously.

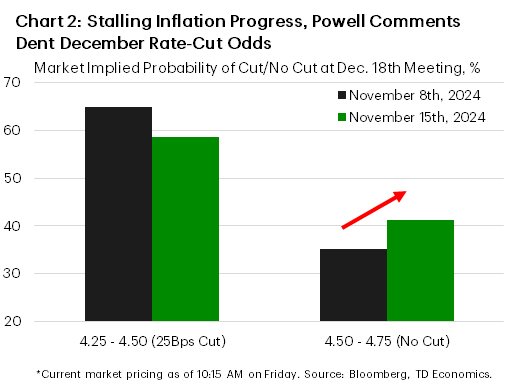

The inflation data, combined with Powell’s comments appeared to move markets, sending yields and the dollar moderately higher, while taking a toll on equities. Market odds for the Fed to take a pause on rate cuts have surged higher in recent days, with a probability of a little over 40% (Chart 2). The next payrolls report should be pivotal for the Fed heading into the December meeting, but given that it may continue to show volatility from one-off factors (i.e., recent hurricanes), the Fed will still have its work cut out for it in trying to ascertain the underlying strength in the labor market.

Next week’s economic calendar sees updates on housing in October, which are not likely to show the impact from the recent upswing in mortgage rates yet. The starts data could be messy due to hurricane impacts, while existing home sales are still expected to be solid.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.