Financial News Highlights

- The embattled ISM Manufacturing Index showed improvement in November, but continued to point to contraction in financial news. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed.

- As was widely expected, hiring rebounded in November, with payrolls adding 227,000 new jobs, as impact of the Boeing strike and hurricanes reversed. However, an uptick in the unemployment rate increased market confidence that a Fed rate cut is in the offing.

- Vehicle sales also posted a sizeable gain in November, reaching the highest level in over three years. It is possible that some of this strength in sales came from replacement demand related to hurricane activity.

Data Clears the Path for the Rate Cut in December

It’s not just the Christmas holidays that are fast approaching. The next Federal Reserve meeting is also just around a corner, and this week featured several important updates for signals on the health of the U.S. economy. This week’s results were broadly positive: contraction eased in manufacturing, activity continued to expand in the services sector, job growth rebounded in November, as did vehicle sales. Vehicle sales registered their highest level in over three years, although it is possible that some of this strength came from replacement demand related to hurricane activity.

It’s not just the Christmas holidays that are fast approaching. The next Federal Reserve meeting is also just around a corner, and this week featured several important updates for signals on the health of the U.S. economy. This week’s results were broadly positive: contraction eased in manufacturing, activity continued to expand in the services sector, job growth rebounded in November, as did vehicle sales. Vehicle sales registered their highest level in over three years, although it is possible that some of this strength came from replacement demand related to hurricane activity.

The embattled ISM Manufacturing Index showed improvement in November, but still signaled that activity is contracting. Overall, the manufacturing sector has gained some momentum, with the new orders index rising for the third consecutive month, since the Fed began cutting interest rates. However, regulatory and trade policy cloud the outlook. In contrast to manufacturing, the services sector continued to expand in November, although the pace of growth slowed. Still, with 14 out of 18 industries reporting growth, the services sector appears to be in relatively good shape.

As expected, hiring rebounded in November, with payrolls adding 227k new jobs in financial news (Chart 1). Revisions also added 56k jobs to the gains seen in the prior two months. Smoothing through the recent volatility, job gains have averaged 173k over the past three-months, or only a modest step down from the 186K averaged over the prior twelve-month period. But this likely overstates the degree of “strength” in the job market. In the household survey, the unemployment rate backed up one tenth to 4.2%, after spending September and October at 4.1%.

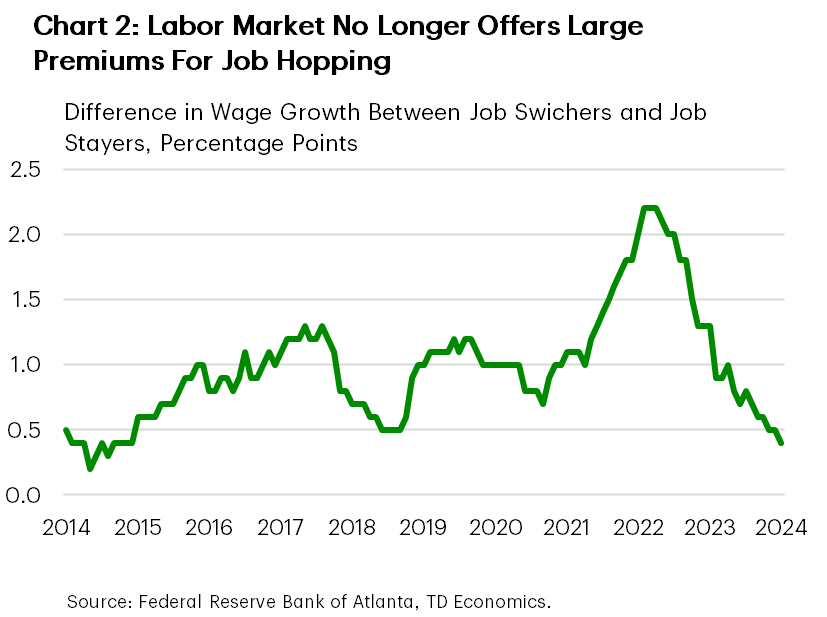

Other indicators, such as the Job opening and labor turnover survey (JOLTS), similarly point to a labor market that has come into balance and is no longer a meaningful source of inflationary pressure. JOLTS data, released this week, showed that while job openings increased in October, the uptick was narrowly concentrated in professional and business services and leisure and hospitality. Meanwhile, both the quit rates and the hiring rate are below their pre-pandemic levels. This suggests that the employers are becoming more selective, while workers are less eager to leave job voluntarily. Indeed, with no significant premium for job switching (Chart 2) and given the low hiring rate, landing a new job may be challenging.

Other indicators, such as the Job opening and labor turnover survey (JOLTS), similarly point to a labor market that has come into balance and is no longer a meaningful source of inflationary pressure. JOLTS data, released this week, showed that while job openings increased in October, the uptick was narrowly concentrated in professional and business services and leisure and hospitality. Meanwhile, both the quit rates and the hiring rate are below their pre-pandemic levels. This suggests that the employers are becoming more selective, while workers are less eager to leave job voluntarily. Indeed, with no significant premium for job switching (Chart 2) and given the low hiring rate, landing a new job may be challenging.

Comments from the latest Fed’s Beige book also reflected this trend, stating that “hiring activity was subdued as worker turnover remained low” and that “wage growth softened to a modest pace”. The Beige book, along with the payrolls and especially the next week’s inflation report will help to solidify the Fed’s stance on their next rate move later this month. The cooling labor market should give the policy makers confidence for another quarter point cut. However, with inflation showing some stickiness lately, and in the words of Jerome Powell this week, the Fed could “afford to be a little more cautious”. The market is pricing nearly 90% odds of a December cut, but the path for rate cuts in 2025 is less clear (report).

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.