Financial News Highlights

- The U.S. economy ended 2024 on solid footing, expanding at a 2.3% annualized pace. The consumer did the heavy lifting, with spending accelerating in the fourth quarter.

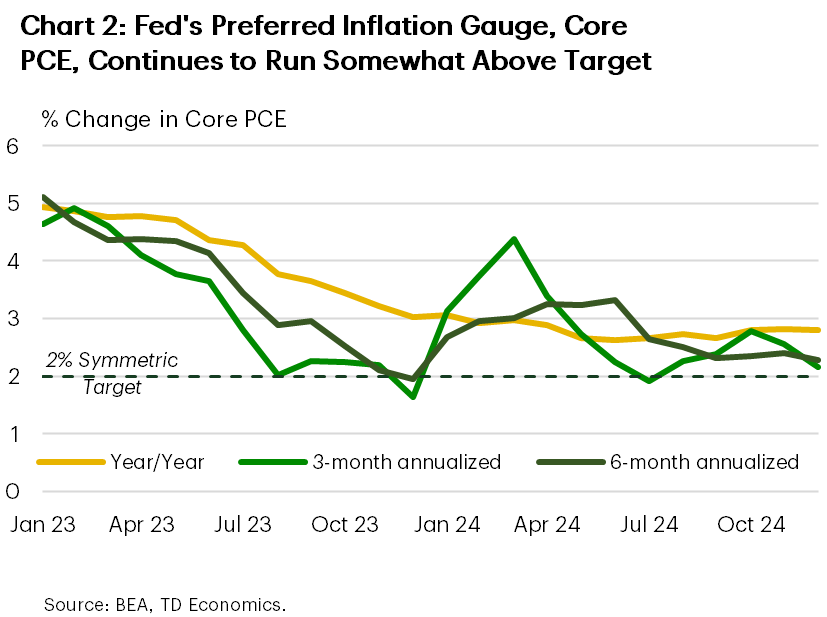

- The Fed’s preferred inflation gauge, the core PCE deflator, continued to hover somewhat above target in December, growing at 2.8% year-on-year. But trends over the past few months suggest further cooling ahead.

- Major action may come on the trade policy front as early as this weekend, with President Trump reiterating his intentions to impose tariffs on Canada and Mexico – America’s largest trading partners.

U.S. – Stock Market Rowdy, Economy Steady

The last week of January began on a soft note for stock markets in financial news. As it became apparent that a low-cost Chinese artificial intelligence start-up (DeepSeek) could threaten the dominance of American rivals, the valuations of several large tech firms took a hit, weighing on major indexes. Some recovery ensued later in the week, with the S&P 500 and tech-heavy NASDAQ nearly erasing the losses from last week’s close (at the time of writing). In contrast to the rowdiness of the stock market, signals out of the economy continued to point to steadiness.

The last week of January began on a soft note for stock markets in financial news. As it became apparent that a low-cost Chinese artificial intelligence start-up (DeepSeek) could threaten the dominance of American rivals, the valuations of several large tech firms took a hit, weighing on major indexes. Some recovery ensued later in the week, with the S&P 500 and tech-heavy NASDAQ nearly erasing the losses from last week’s close (at the time of writing). In contrast to the rowdiness of the stock market, signals out of the economy continued to point to steadiness.

The first read on fourth quarter GDP showed that the U.S. economy ended last year on a solid footing as it grew at 2.3% quarter-on-quarter annualized. The consumer did the heavy lifting, offsetting a notable drag from gross fixed private investment (Chart 1). Goods spending carried the torch once again, propelled forward by a double-digit increase in durable goods, but services also notched a mild acceleration. Meanwhile, within the softness of the broad private investment category, residential investment was a bright spot for a change, lifted by a double-digit gain in housing starts last quarter. Looking at the big picture, the fact that the economy essentially sustained 2023’s pace through 2024, despite the still elevated interest rate environment, is an impressive accomplishment.

Friday morning’s monthly PCE report provided some more detail with respect to consumption and inflation trends at the turn of the year. The handoff to the start of 2025 is solid, as real spending growth remained robust in December, growing at nearly 5% annualized. This, as strength in services helped offset some cooldown in goods spending from the double-digit gain in the month prior. Additionally, the Fed’s preferred inflation gauge – core PCE – held at 2.8% in year-on-year terms. The fact that the 3-month and 6-month annualized rate of change in core PCE inflation gravitated lower toward the target, was a welcome development (Chart 2).

With inflation still somewhat elevated (though appearing to head in the right direction) and the economy remaining on solid footing, the Fed can afford to take a cautious approach to further loosening monetary policy. The FOMC left the policy rate unchanged at this week’s meeting – a move that was widely anticipated. Fed Chair Powell acknowledged that “we don’t need to be in a hurry to adjust our policy stance”, while nodding to the uncertainties and the risks related to major policy changes out of Washington, such as on trade policy. Powell reiterated a wait-and-see approach, stating that they’d need any new policy changes to be articulated first, before assessing their impacts on the economy in financial news.

With inflation still somewhat elevated (though appearing to head in the right direction) and the economy remaining on solid footing, the Fed can afford to take a cautious approach to further loosening monetary policy. The FOMC left the policy rate unchanged at this week’s meeting – a move that was widely anticipated. Fed Chair Powell acknowledged that “we don’t need to be in a hurry to adjust our policy stance”, while nodding to the uncertainties and the risks related to major policy changes out of Washington, such as on trade policy. Powell reiterated a wait-and-see approach, stating that they’d need any new policy changes to be articulated first, before assessing their impacts on the economy in financial news.

Major action on the trade front may come as early as this weekend, with President Trump reiterating his intention to impose 25% tariffs on Mexico and Canada on February 1st. There’s still a possibility that cooler heads will prevail, as President Trump’s top pick for commerce secretary suggested that tariffs could be avoided if swift action was taken on the border issues. Still, the deadline is fast approaching and any trade skirmishes with its neighbors will be problematic – the two countries are America’s largest trading partners and are deeply integrated in supply chains.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.