Financial News Highlights

- President Trump announced a universal 25% tariff on all steel and aluminum imports, effective March 12th in financial news.

- January CPI came in hotter than expected, with core inflation rising at its fastest monthly pace since March 2024.

- Speaking at a semiannual congressional hearing, Chair Powell emphasized that policymakers were in no rush to cut rates.

Hot CPI + Trade Uncertainties = Extended Fed Pause

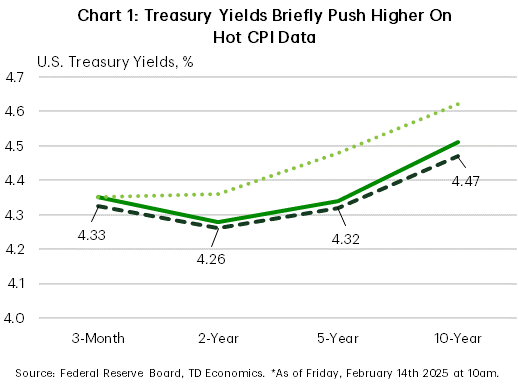

Tariffs remained the policy focus of the new administration this week, with President Trump announcing a universal 25% tariff on all steel and aluminum imports into the U.S., effective March 12th. Financial markets were largely unperturbed by the announcement, perhaps because the more targeted measures hinted towards a broader pivot on how the administration planned to implement its tariff agenda. But a hotter-than-expected CPI reading for January and a firm commitment from Chair Powell that policymakers were in no hurry to cut rates, helped to temporarily sour the mood by mid-week. Treasury yields across the curve briefly pushed higher only to completely retrace on Thursday, as President Trump’s threat of announcing further reciprocal tariffs showed no immediate action. The S&P 500 ended the week 1.6% higher, while Treasury yields were largely unchanged, with the 10-year currently sitting at 4.47% (Chart 1).

Tariffs remained the policy focus of the new administration this week, with President Trump announcing a universal 25% tariff on all steel and aluminum imports into the U.S., effective March 12th. Financial markets were largely unperturbed by the announcement, perhaps because the more targeted measures hinted towards a broader pivot on how the administration planned to implement its tariff agenda. But a hotter-than-expected CPI reading for January and a firm commitment from Chair Powell that policymakers were in no hurry to cut rates, helped to temporarily sour the mood by mid-week. Treasury yields across the curve briefly pushed higher only to completely retrace on Thursday, as President Trump’s threat of announcing further reciprocal tariffs showed no immediate action. The S&P 500 ended the week 1.6% higher, while Treasury yields were largely unchanged, with the 10-year currently sitting at 4.47% (Chart 1).

The steel and aluminum tariffs announced on Monday come just a week after Canada and Mexico were able to get a 30-day delay on the blanket 25% tariffs that were supposed to go into effect on February 1st. But unlike those tariffs, the administration has some historical precedence for the steel and aluminum tariffs, with President Trump having enacted similar measures back in 2018/19. For most countries, the previous tariffs had been lifted. However, this week’s announcement would reinstate the 25% tariff on steel and ups the tariff on aluminum to 25% (previously 10%), with no country exemptions.

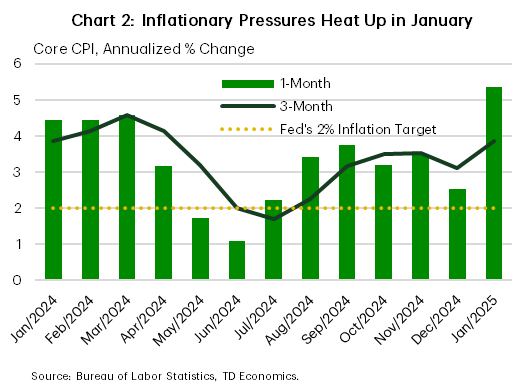

The ratcheting up of trade tensions has come at particularly challenging time for policymakers, as the Fed’s fight to return price stability has hit a wall. The January CPI reading showed headline inflation rising at its fastest monthly pace in nearly a year and a half, while core inflation’s gain was the largest since March 2024 (Chart 2). Residual seasonality looks to be at least partially responsible for January’s uptick – as it was in the early months of last year. This appears to be a legacy issue stemming from the pandemic.

The ratcheting up of trade tensions has come at particularly challenging time for policymakers, as the Fed’s fight to return price stability has hit a wall. The January CPI reading showed headline inflation rising at its fastest monthly pace in nearly a year and a half, while core inflation’s gain was the largest since March 2024 (Chart 2). Residual seasonality looks to be at least partially responsible for January’s uptick – as it was in the early months of last year. This appears to be a legacy issue stemming from the pandemic.

Historically, businesses tend to build in big price adjustments at the beginning of each year, which would normally be corrected for with appropriate seasonal factors. But during the COVID pandemic, firms were much faster to pass on price increases, distorting the seasonal patterns, and biasing the January inflation readings higher in recent years in financial news.

But it’s unlikely that residual seasonality is telling the whole story. Consumer spending remained incredibly strong through the second half of last year – averaging an impressive 3.6% annualized. Moreover, spending on both goods and services was very healthy in Q4, helping to explain the breadth of price pressures last month. While the January retail sales data point to a sharp slowing in spending, those figures were likely impacted by inclement weather and the California wildfires – suggesting some giveback in spending in February.

At this point, the Fed appears to have plenty of runway to maintain its current policy rate and wait for more clarity on the inflation front. This is unlikely to come with just the next few inflation readings, which means the Fed is on hold until at least the summer.

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered. Do you have any questions about your finances? As financial advisors in Cornelius NC, Naples FL, and Moultonborough NH we are happy to help.

To see more news reports, click here.