Determining When to Take Social Security Benefits

The benefits of postponing until your full retirement age

Social Security is an asset that is taken for granted by many folks. If you are tempted to take Social Security early, when first eligible at age 62, think again: your check will be lower if you don’t wait until what’s called full retirement age. Further, married couples benefit additionally from Social Security planning strategies that can provide additional income.

The Social Security Administration is not allowed to advise on strategies to maximize your benefits, so don’t expect to learn about this from the government. But a financial advisor can help you determine how long you should work and what you should do in retirement to avoid outliving your assets.

Before You Make a Decision

As with everything in life, there are advantages and corresponding disadvantages to every decision and that is true when you are deciding whether or not to take your social security benefits before your full retirement age. On the one hand, if you do take your benefits before your full retirement age, then you can collect benefits for a longer period of time. How much longer? Well, that answer is unknown, unless you for sure know your life expectancy.

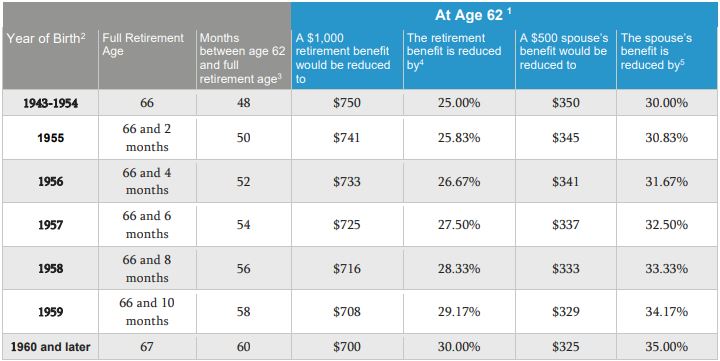

The disadvantage to taking your retirement benefits before your full retirement age is that your benefits will be reduced. Reduced by how much? Take a look at the chart below to find out.

The decision on when to take your social security benefits is a personal one – there is no “perfect age” for everyone. But remember that when you decide to take your social security benefits, the amount you receive when you first get benefits will set a baseline for the amount you will receive for the rest of your life.

So you need to ask yourself at least these three questions:

- Do I plan to continue working?

- How is my health?

- Are there other family members qualifying for benefits based on my decision?

Full Retirement and Age 62 Benefit by Year of Birth

Speak with an Advisor

Again, the Social Security Administration is not allowed to advise on strategies to maximize your benefits, but a financial advisor is. A financial advisor can run different retirement scenarios based on different variables such as: where you are today, how long you might work, projected rates of returns, and future living expenses, while also factoring in rising health care costs, among other things. Ultimately, the decision is, of course, yours. However, a financial advisor can help you make the most informed decision based on your personal goals and objectives.

Click here to speak with an advisor today.

1 You must be at least 62 for the entire month to receive benefits

2 If you were born on January 1st, you should refer to the previous year.

3 If you were born on the 1st of the month, we figure your benefit (and your full retirement age) as if your birthday was in the previous month. If you were born on January 1st , we figure your benefit (and your full retirement age) as if your birthday was in December of the previous year.

4 Percentages are approximate due to rounding.

5 The maximum benefit for the spouse is 50 percent of the benefit the worker would receive at full retirement age. The percent reduction for the spouse should be applied after the automatic 50 percent reduction. Percentages are approximate due to rounding

“Open Enrollment Season is Around the Corner”. FMEX 2020.https://fmexcontent.s3.amazonaws.com/1289/1289.pdf

This material is for informational purposes only. It should not be considered a comprehensive financial plan or investment recommendation. Please consult a qualified financial advisor before making decisions about your personal financial situation.