FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

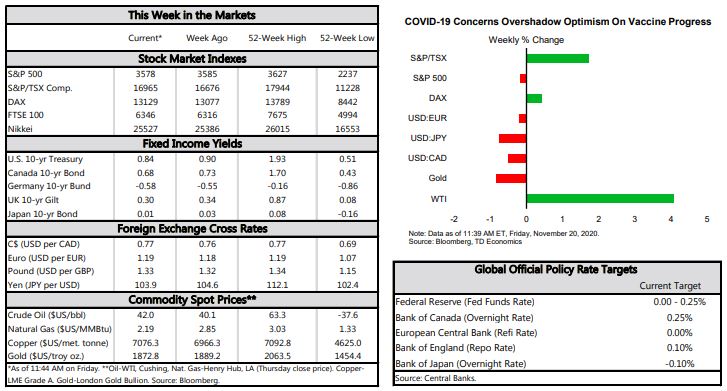

- COVID-19 concerns took center stage again this week as cases surged to new daily records. This overshadowed optimism on vaccine progress and mostly positive economic data, with U.S. equity markets trending modestly lower as a result.

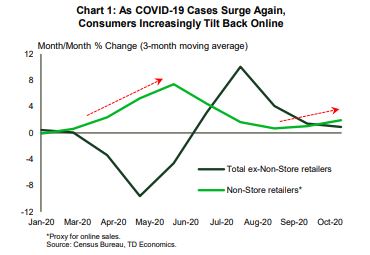

- Retail sales grew by 0.3% in October, extending their winning streak. Housing market data meanwhile continued to surprise on the upside, with existing home sales up 4.3% on the month and housing starts up 4.9%.

- Signals from the labor market were not quite as upbeat, with initial jobless claims recording a mild increase to 742k last week from 711k the week earlier.

It’s Always Darkest Before the Dawn

Concerns around the spread of COVID-19 took center stage once again this week as infections surged to new records. Optimism over vaccine progress and broadly positive economic data generally played second fiddle. Equity markets trended modestly lower on the week as a result.

On the economic data front, retail sales improved by 0.3% in October, extending their winning streak to six months. The outturn, however, was below market expectations and a marked deceleration in the pace of gains from the 1.5% averaged in the three months prior. Within this slowing trend, there’s a noticeable shift toward online shopping. Sales at non-store retailers, a proxy for online sales, appear to be taking the lead once again as in-store sales moderate – a divergence that is in line with the third wave of COVID cases (Chart 1).

Home sales, meanwhile, continued to be robust in October. Existing home sales defied market expectations, rising by 4.3% (Chart 2). The growth in resale activity over the past several months has been nothing short of remarkable. Sales are now up nearly 27% from year-ago and 19% from the pre-crisis peak. The number of homes for sale, on the other hand, is in short supply. At the current sales pace, there is just 2.5 months of supply on the market – a record low. With such little product for homebuyers to choose from, the median sales price accelerated further, to 15.5% year-over-year. The strong acceleration in home price growth has overwhelmed the positive impact of record-low mortgage rates on housing affordability. The combination of deteriorating affordability and low supply is likely to lead to a more moderate pace of sales growth going forward.

The good news is that new supply does appear to be responding to these market forces. With builder confidence riding high, housing starts also defied expectations in October, rising a better-than-expected 4.9%. The increase was driven entirely by single-family starts – a clear signal of the shift in housing preferences during the pandemic.

Signals from the labor market were not as upbeat. While continuing jobless claims trended lower at the beginning of the month, initial jobless claims recorded a mild increase to 742k last week from 711k the week earlier. The still-elevated level of initial claims, a proxy for layoffs, points to softer labor market momentum. The rising spread of COVID-19 is an added near-term risk. With hospitalizations also trending higher, several jurisdictions throughout the U.S. are leaning more heavily on containment measures, which will weigh on business activity and hiring. What’s more, with the virus spreading out of control, stronger measures, such as lockdowns, cannot be ruled out for some parts of the country.

With more containment measures, no new fiscal supports, and the expiry of several Fed emergency lending programs (corporate credit, municipal lending and Main Street Lending programs), the near-term outlook is looking darker. Indeed, it appears that a sustained improvement in economic activity will likely have to wait for a vaccine. Fortunately, there is a light at the end of the tunnel. Major positive developments on the vaccine front in recent days suggest potentially earlier availability and the return to normal in 2021. It’s always darkest before the dawn.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.