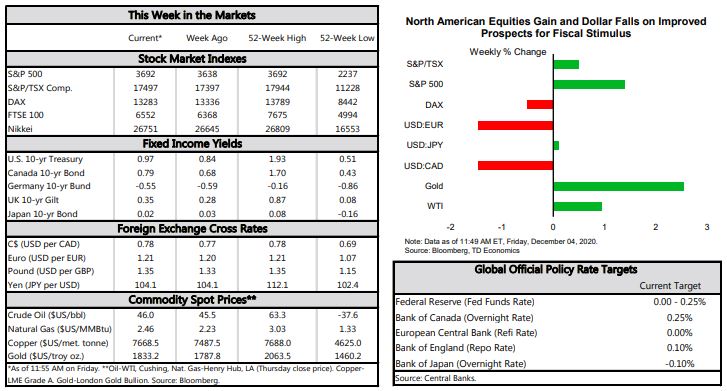

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Financial markets remained upbeat this week, looking past the near-term risks associated with the ongoing health crisis.

- Economic data delivered a mixed bag. Both ISM activity indexes remained in expansionary territory and jobless claims showed improvement, but nonfarm payrolls disappointed with lower-than-expected gains in November.

- The surge in infections is expected to continue until early January. Fortunately, prospects for additional fiscal supports brightened this week, which would go a long way to supporting the recovery into the New Year

U.S. – December Calm Before the Storm

The first week of December brought a mixed bag of economic and financial data. On the financial front, the S&P 500 continued to defy gravity, setting a record high almost every day of the week despite soaring cases of coronavirus infections and related deaths. Markets looked past the near-term risks associated with the continued health crisis and focused on the positives. The “reopening trade” that started with positive vaccine news continued into the fourth week, while renewed hopes of an additional fiscal package added fuel to the fire. The likelihood of a deal before the end of the year improved this week, as news broke of a $908 billion compromise offered by a bipartisan group of Senators.

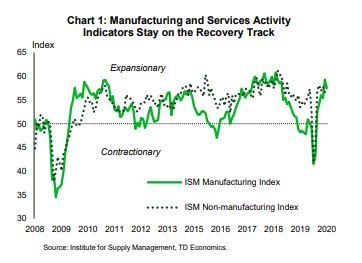

On the economic side, the data was rich this week. The Institute for Supply Management released November updates for its manufacturing and non-manufacturing purchasing managers indexes. Both indexes posted moderate declines but remained in expansionary territory, indicating a slowing but still positive pace of improvement (Chart 1). The slowdown in manufacturing was driven by new orders, production and inventories, while the employment sub-index moved back into contractionary territory just one month after posting an above-50 reading in October. Overall, the index remains at the high end of historical readings, suggesting that manufacturing demand remains strong for most sectors. The recovery in services, meanwhile, continued for the sixth month in a row despite increased restrictions across several states in November. Sectors sensitive to social distancing measures remain in contraction and are unlikely to get a recovery boost until more progress is achieved in defeating the pandemic.

On the employment front, the data was mixed. Last week’s jobless claims declined after a two-week consecutive increase. However, the reading may be overstated due to processing complications during the Thanksgiving holiday. To make matters worse, the weekly claims report came under scrutiny due to a GAO report noting “flawed estimates of the number of individuals receiving benefits.”

The November nonfarm payrolls report was more in tune with the epidemiological data. Employment rose by 245k – roughly half the amount that economists expected. Employment gains were particularly modest in the leisure and hospitality sector, which remains one of the most badly hit sectors of the economy (Chart 2). The unemployment rate fell to 6.7% from 6.9% but was marked with a sizeable decline in the labor force. The number of people not counted as unemployed but who want a job rose by almost 450 thousand to 7.1 million, 2.2 million more than in February 2020.

Moderate employment data provides more evidence of a bifurcated recovery, suggesting that more relief measures are required to support American households that are struggling in this pandemic. According to the most recent Household Pulse Survey 32% of families reported some difficulty paying for usual household expenses during the coronavirus pandemic. As the surge in infections is not expected to wane until at least early January, there is a strong case for additional fiscal supports. Fingers crossed the message appears to be getting through.

Maria Solovieva, CFA, Economist | 416-380-1195

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.