FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The first full week of the second quarter was sparse on economic data. The service sector showed signs of modest acceleration, while vehicle sales declined for the second consecutive month in March.

- The Federal Open Market Committee (FOMC) March meeting minutes reiterated members’ unwavering commitment to moving fast to restore price stability.

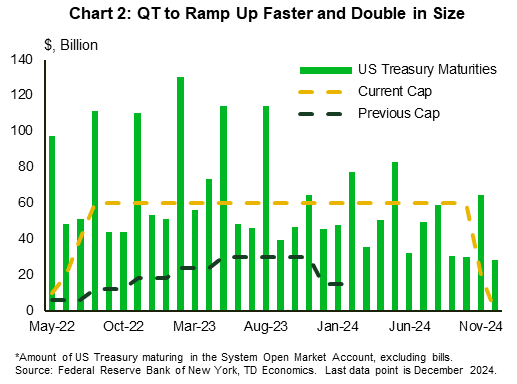

- The minutes provided a blueprint of the Fed’s balance sheet runoff, which will be more aggressive and ramp up faster than before. At such pace, the runoff should finish by the end of 2024.

U.S. -The Fed’s Most Important Task

The first full week of the second quarter was sparse on economic data in financial news. On Tuesday, the Institute for Supply Management released its report on services that provided signs of modest acceleration in economic activity in the sector. Still, the report was full of contrasting elements. On the one hand, demand indicators were higher with business activity, and both new domestic and export orders up on the month. This was likely supported by stronger employment and the recent improvement in delivery times allowing businesses to rebuild depleted inventories.

On the other hand, the imports sub-index fell into a contractionary territory while ongoing supply chain issued lowered purchasing managers’ inventory sentiment to an all-time low. The prices paid indicator was unsurprisingly higher given the energy shock dealt by the Russia-Ukraine war with all 18 industries reporting higher prices (Chart 1). In addition, respondents’ comments were quite negative, reflecting the pessimism over increasing cost and ongoing supply chain disruption.

This pessimism was echoed in the vehicle sales release, which showed the second consecutive month of decline in March. While underlying demand remains strong and improving, sales will remain constrained by limited inventory. Furthermore, production may suffer another blow should the war in Ukraine result in semiconductor shortages later in this year. As a result of strong demand and tight supply, the inventory-to-sales ratio – a measure of adequacy of supply relative to current demand – remains historically low. This will continue to put upward pressure on car prices over the near-term.

Fighting persistent price pressures remains the Fed’s most important task. The Federal Open Market Committee (FOMC) March meeting minutes reiterated members’’ unwavering commitment to moving fast to restore price stability and reach a neutral policy stance by year end. Many participants expressed their concerns about inflationary risk and voiced their preference to tighten the policy rate by 50 basis points at the next meeting on May 3rd-4th.

The minutes also provided a plan for the Fed’s balance sheet runoff (aka Quantitative Tightening or QT). As we wrote in this report, the monthly caps will be larger than in the previous QT cycle, scaled up by the increase in asset holdings (Chart 2). The participants agreed to shed $60 billion Treasury securities and about $35 billion agency MBS monthly, but the phase-in period will be shorter than we expected at just three months. The runoff may start as early as May, which suggests that the balance sheet could shrink by $2.7 trillion by the end of 2024. By this time, we expect that the Fed will reach $1.7 trillion in reserves – the level of reserves “consistent with the Committee’s ample-reserves operating framework”.

Bond markets reacted by selling longer-dated US Treasury securities, which led to yield-curve steepening. At the time of writing, the 10-year Treasury yield was at 2.69% – up 0.3 percentage points relative to where it closed last week.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.