FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Another solid jobs report showed that the U.S. economy added 431k jobs in March. Wage growth picked up and the unemployment rate fell 0.2 percentage points to 3.6%.

- President Biden presented a $5.8 trillion budget to Congress with a hefty focus on defense spending. Separately, the President also announced releases from the strategic petroleum reserve to combat rising energy prices.

- Nominal consumer spending and income rose in February. Real income, however, pulled back as prices rose rapidly. Inflation, as measured by the year-on-year percent change in the personal consumption price index accelerated to 6.4%.

U.S. -Economic Recovery Battles Inflation Headwinds

On the agenda this week in financial news were several important data releases including consumer income and spending, manufacturing activity, and the March employment report. President Biden also released his budget proposal and announced a plan to release supply from the strategic petroleum reserve in order to combat rising prices.

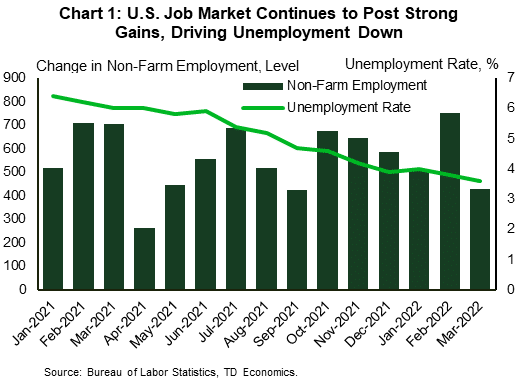

Jumping right in, nonfarm payrolls expanded by 431k in March with most sectors posting job gains. The only exceptions were transportation & warehousing and utilities. The unemployment rate edged down to 3.6% from 3.8% in February as household employment growth exceeded growth in the labor force (Chart 1). Wages continued to post solid year-on-year growth, ticking up from 5.1% in February to 5.6%. Overall, the report indicates a job market driving full steam ahead, and barring further disruptions, could be back to its pre-pandemic level of employment by the middle of the year.

The ISM Manufacturing Index indicated that factory activity, while still expanding, slowed in March. The index pulled back to 57.1 from 58.6 the month before. There were notable declines in new orders and an increase in prices paid. On the upside, the backlog of orders declined, while the employment index rose.

Turning to the household sector, nominal personal income and spending rose 0.5% and 0.2% respectively in February. An even stronger gain in prices however took a bite out of real disposable income, which declined for the third consecutive month, largely reflecting waning transfers to households. Inflation, meanwhile, continued to accelerate. The personal consumption expenditure (PCE) index rose 6.4% year-over-year (y/y) versus 6.1% in January (Chart 2). The core PCE index also accelerated to 5.4% y/y in February, up from 5.2%. From the Fed’s perspective, inflation is uncomfortably high as supply chains remain stressed, Covid shutdowns in China hamper trade and the Russian-Ukraine war sparks further volatility.

In response to rising energy prices, President Biden plans to release up to 180 million barrels of oil from the strategic reserve over the next six months. While the release may help to alleviate near-term market tightness, the reserve is currently at a 20-year low. Further releases would drive the stockpile even lower, ratcheting up risks surrounding global spare capacity over the longer term.

Finally, President Biden presented his budget proposal for the 2023 fiscal year. The $5.8 trillion budget would raise taxes on billionaires and corporations. A new tax proposal would require households worth more than $100 million to pay a rate of at least 20% on their income as well as a tax on unrealized capital gains on assets such as stocks, bonds, or privately held companies. On the spending side, the budget would increase spending on the military, law enforcement, affordable housing and supply chains, while attempting to reduce the federal deficit by $1 trillion over a decade.

Shernette Mcleod, Economist | 416-415-0413

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.