FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- In a carefully crafted speech this week in D.C., Fed Chair Powell reaffirmed the Fed’s keenness for a more aggressive removal of monetary stimulus in order to restore price stability.

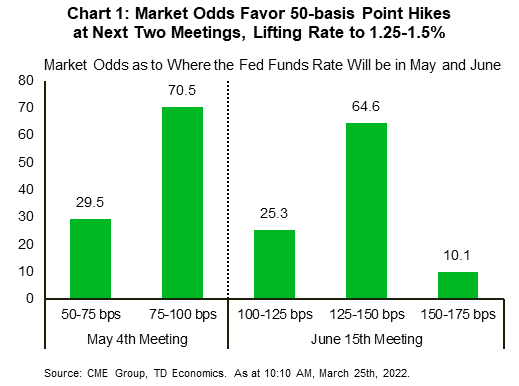

- Powell highlighted the potential for the Fed to go with hikes larger than 25 basis points (bps) if deemed appropriate. Market odds now heavily favor 50 bps hikes at the next two FOMC meetings in May and June.

- On the data front, both new single-family home sales and pending (existing) home sales pulled back in February.

U.S. -Fed’s Focus Tilts Squarely on Restoring Price Stability

If last week’s Fed rate hike (and a sharp move up in the number of future expected hikes among FOMC members) left any doubt about the Fed’s transition to a more hawkish stance, Powell’s remarks this week are likely to have sealed the deal in financial news. There was no shortage of Fed speeches to parse, in a week that didn’t have much in the way of data.

The most noteworthy speech was Fed Chair Powell’s remarks in D.C. on Monday. Reading carefully crafted remarks, Powell recognized that the labor market is strong and still has “substantial momentum”. Further driving home his point, last week’s jobless claims fell to the lowest level since 1969. Powell also noted that inflation is “much too high” and touched on the fallout from the Russia-Ukraine conflict, which will put additional upward price pressure through several key commodities, including crude oil. The price of the latter is up from last week and is holding near $110 per barrel at time of writing – a level that is broadly in line with our recent forecast (see here). Powell also emphasized that the path of inflation remains uncertain. He pointed out the potential for more COVID-related supply chain disruptions out of China, where a rise in Covid infections led to the lockdown of another major city of nine million people this week.

On the monetary policy response, Chair Powell noted that the Fed would not assume significant near-term supply-side relief on inflation but would instead be looking for actual progress on the ground. This was followed by more hawkish comments regarding the size of rate hikes, with the Chair highlighting the potential for the Fed to go with hikes larger than 25 basis points (bps) if deemed appropriate. Powell went further, stating that if the Fed determines the need to “tighten beyond common measures of neutral and into a more restrictive stance”, it will do that as well. This was already shown in the Fed’s updated dot plot, which had a median projected policy rate of 2.8% in 2023-24, above the long-run rate of 2.4%.

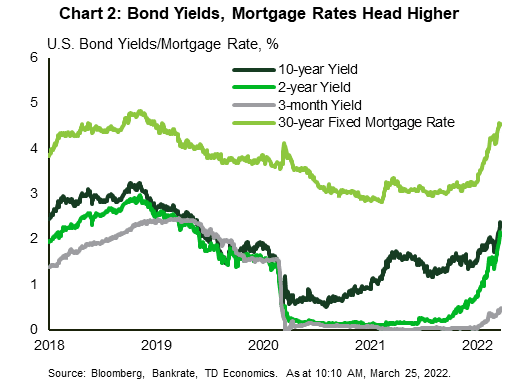

Several other Fed officials, including Mester, Daly, and Evans, echoed the hawkish stance by showing more comfort with rate hikes larger than a quarter point. It comes as no surprise then that market odds are now heavily favoring 50 bps hikes at the next two policy meetings (Chart 1). Bond yields and mortgage rates, meanwhile, continued to head higher (Chart 2). Thirty-year mortgage rates rose above 4.5% this week – a sharp increase from a little over 3% at the start of the year. Higher interest rates will take some steam out of housing demand this year, with this week’s declines in new and pending home sales for the month of February not entirely surprising in financial news. Higher borrowing costs are part of the reason why we expect the housing market to cool this year. For more on our housing outlook see here.

The bottom line is that the Fed is behind the curve on inflation, and now needs to take stronger steps to rein it in. While this also increases the chances of policy error, the Fed has reaffirmed its keenness for a more aggressive removal of monetary stimulus to restore price stability.

Admir Kolaj, Economist | 416-944-6318

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.