FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets this week have been largely driven by corporate earnings and political events, with tensions on the Korean Peninsula escalating to the point where markets can no longer ignore them.

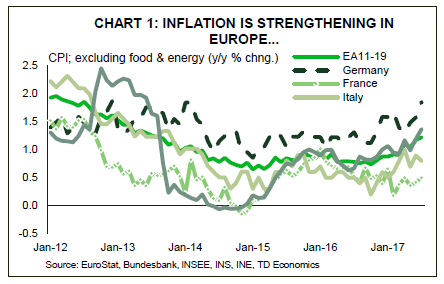

- Inflation strengthened in the Eurozone, with prices growing by 0.13% in July and the year-over-year measure accelerating to 1.2% with strength particularly apparent in Germany and Spain.

- U.S. inflation surprised to the downside once again, with prices growing by 0.1% in July – or half the expected pace. Despite the soft CPI print and PPI figures, we expect inflation will strengthen somewhat in the coming months.

Inflation Strengthens in Eurozone, But Stays Soft in U.S.

Markets have this week been driven largely by political events and corporate results. Second quarter earnings continued to impress, boosting sentiment and stock valuations. Oil prices also helped, with the WTI benchmark rising above $50 on Thursday morning, helped along by rising global tensions and a drawdown in US inventories.

Escalating tensions really begun to weigh on markets on Thursday afternoon with stock indices having the worst day in three months. Volatility sprung to life, with the VIX rising to 17. The tensions have so far boosted the flow of money into safe-haven assets, such as G7 government bonds. At the same time, risk assets exposed to the peninsula, such as the Kospi, Shenzen, and Nikkei equity indices fell on the week. While we don’t expect situation on the Korean Peninsula to result in armed conflict, it could lead to weaker economic performance as consumers and businesses in the region pare back spending.

As far as economic data, this week was all about inflation. The story was relatively good in Europe, with several economies seeing robust readings. Core CPI in Germany and Spain rose by 0.4% and 0.3% (m/m) in July – the fastest monthly pace of several years. Price gains in France and Italy were less apparent, and averaged 0.13% for the Eurozone as a whole. Still, inflation in year-on-year terms accelerated to a four-year high of 1.2%, with these readings likely to provide further comfort for ECB officials to begin considering paring back on bond buying.

Inflation was far less robust in the U.S. with the producer price index (PPI) report on Thursday as well as its consumer cousin a day later, underwhelming. Total PPI declined 0.1%, marking its first decrease in eleven months, while the core measure pulled back by just as much in July, with the year-on-year measures decelerating by 0.3 percentage points to 1.9% and 1.8%, respectively. The consumer price index (CPI) also missed expectations, increasing by half of the 0.2% m/m gain that was expected.

There are reasons to be hopeful. This week’s NFIB survey offered some reassurance, with the share of firms raising selling prices rising to 8% – the highest share since mid- 2014. There was also an increase in the share expecting to raise prices from 19% to 23%. At the same time, labor market progress continues at a resilient pace. With unemployment at 4.3%, wages growing at 2.5% y/y, and the trade-weighted dollar down 8% from its peak in December, inflation is likely to turn higher in the months ahead. This should allow the Fed to continue its plans to normalize its balance sheet and perhaps sneak in one rate hike before the year is out.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.