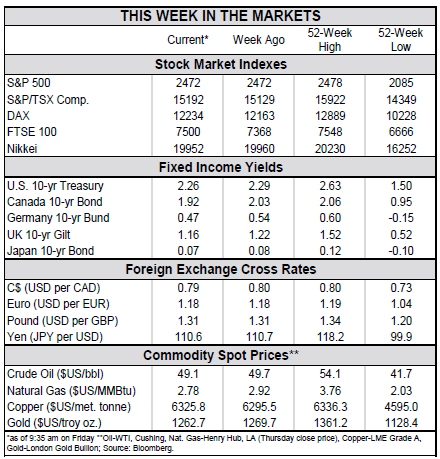

HIGHLIGHTS OF THE WEEK

- U.S. stock indices remained supported by the continued flow of favorable earnings releases. Bond yields and the U.S. dollar moved lower through Thursday, but that dynamic reversed course with the robust payrolls report.

- The American economy continued to churn out jobs at a robust pace in July with payrolls rising by 209k. At the same time, the unemployment rate fell to a cycle low of 4.3%. Average wages rose a solid 0.3% m/m.

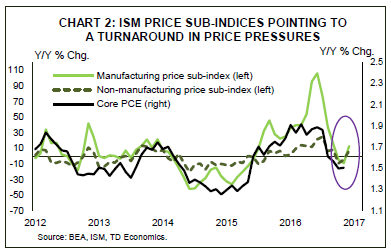

- Improvements in ISM manufacturing and non-manufacturing prices sub-indices, together with a slightly firmer core PCE price index suggest that a turnaround in inflation may be underway.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

Jobs Numbers Impress, But Still Waiting on Inflation

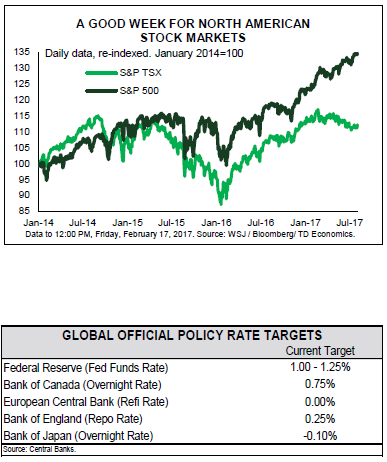

It was another good week across most markets. U.S. stock markets remained supported by continued flow of favorable earnings releases, with the DJIA breaching the 22,000 threshold by mid-week. A string of softer data releases through Thursday also led bond yields and the U.S. dollar lower. But that ended Friday morning, when a solid employment report boosted the dollar and inspired a bit of a sell-off in the bond market.

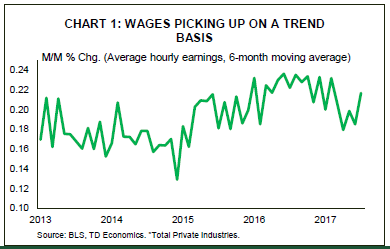

The report was indeed a beauty as the American economy continued to churn out jobs at a robust pace in July, with payrolls rising by 209k, beating market expectations for a 180k print. But there was more. The jobless rate dropped to a cycle low of 4.3%, while broader measures of labor underutilization remained near their pre-recession lows. More workers joined the labor force, with the participation rate recording a small uptick to 62.9%. While average wages failed to accelerate on a year-over-year basis (Chart 1), given the weakness at the beginning of the year, the monthly gain of 0.3% was very strong and marks the fastest pace in ten months. Going forward, we expect job gains to slow somewhat. However, the trend should also be accompanied by stronger wage gains. While the relationship between labor market slack and inflation has become more muted in recent years, and is taking longer to materialize, we believe the link still holds. As such, we believe that a pick-up in inflation should materialize before the end of the year, with the stronger data motivating the Fed to take interest rates higher (see report).

The ISM surveys provided mixed signals of the economy. The manufacturing index suggested that the sector continued to expand at a healthy, but slightly slower pace, supported by a rebounding global economy and the lower U.S. dollar. The non-manufacturing index also telegraphed a deceleration in activity, but remained in expansionary territory while most industries continued to report growth. Importantly, both ISM surveys indicated significant increases in their prices sub-indices. Together with a slightly firmer core PCE price index, which was revised up to 1.5% y/y in June this suggests that a turnaround in price pressures could be underway (Chart 2). Should this in fact be the case, we expect further tightening to take place later this year, with the Fed likely to slip in a December hike. Lack of such evidence, on the other hand, will likely stay the Fed’s hand as far as the hike, but is unlikely to prevent the Fed from starting the balance sheet unwinding process in the fall.

Admir Kolaj, Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.