FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets were in a good mood overall this week, despite no deal in Congress on the next round of assistance. The big political news was Biden’s historic VP pick. With 81 days until the election, the race is on!

- Inflation bounced back more quickly than expected in July, as pandemic related discounting rolled off. Core inflation at 1.6% year on year, remained unthreatening.

- Retail sales continued to improve, albeit by slightly less than analysts were expecting. The big increases due to pent up demand from the closures are in the past, but progress is still being made.

Markets Optimistic Despite No Deal Yet from Washington

On the economic data for July, inflation, as measured by the Consumer Price Index, rebounded more sharply than expected. Core inflation rose 0.6% month-over-month – the largest jump since 1991. The move was largely due to price hikes in areas that had seen significant discounting earlier in the pandemic, like motor vehicle insurance and airline fares (spending categories that also experienced steep declines in sales volumes). The acceleration in price growth has led some to raise the specter of stagflation – where higher inflation takes hold despite low growth. However, we think its bit early for that, given some of the volatility in various categories recently. Core inflation was up a modest 1.6% year-on-year in July, so there is still room for prices to normalize further before inflation gets anywhere near a level that is concerning for the Federal Reserve.

Retail sales continued to improve in July, rising 1.2% on the month. They came in below what markets were expecting, but even in the face of surging infections in many areas of the country, retailers continued to make progress. The pace of the rebound has slowed, now that the initial flurry of pent-up demand after the closures has played out. Many of the major categories are very close to or even above their pre-pandemic level of sales (Chart 1). The hardest hit categories are clothing, restaurants and bars and department stores. Restaurants and bars among the later businesses to open, and in some areas face renewed shutdowns. And demand for clothing is likely low, given many people are staying home in their sweatpants, (it has also been hit by the shift to online retailers).

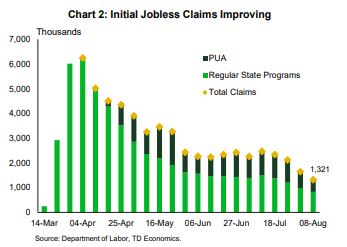

This tally underscores the need for assistance from Washington. Many states’ unemployment benefit rates top out at very low levels: Florida at $275 per week and Arizona at $240 per week. Trump’s executive order funds $300 per week out of FEMA disaster relief funds. But that will likely only last about six weeks. Congress needs to act on another round of relief, particularly for state governments to forestall another round of layoffs at the state and local level which would weigh on growth over the medium term, similar to the dynamic as we saw in the 2010-2012 period.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.