FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Despite a surge in COVID-19 cases in July, economic data remained broadly positive. Vehicles sales rose 11.3% to a better-than-expected 14.5 million (SAAR). The ISM indices also ticked up on the month and beat expectations.

- Importantly, the employment report confirmed that the jobs recovery continued in July, albeit at a slower pace. The U.S. added a better-than-expected 1.8 million jobs, while the unemployment rate fell to 10.2% from 11.1% in June.

- A downward trend in new infections in very recent days marks another positive development. Hopes are also high for a new stimulus package. But, it is unclear if an agreement regarding the stimulus can be achieved in short order.

Historical Decline in GDP As Virus Struck in Q2

Auto sales continued to improve for the third consecutive month in July, rising by 11.3% to a better-than-expected 14.5 million (SAAR) units. In similar fashion, the ISM indices made gains on the month and came in better than expected. The manufacturing index rose 1.6 points to 54.2 in July, with broad-based gains across subcomponents. Its non-manufacturing counterpart did not exhibit the same breadth of gains, but the headline still ticked up one point to 58.1, thanks to a sizable pickup in new orders. While the ISM indices are signaling an expansion at the fastest pace since early 2019, it is important to recall that both sectors are coming out of a very low activity period.

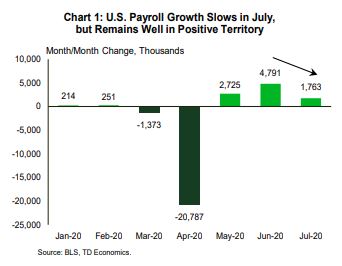

When it comes to gauging the overall health of the labor market, the monthly employment report takes the cake. The July report showed that the recovery in jobs continued last month, albeit at a slower pace (Chart 1). The economy added 1.8 million jobs, beating market expectations. Gains were concentrated in leisure & hospitality, government and retail trade. This brought the three-month tally to 9.3 million, which means that a little over 40% of the jobs lost in the March-April period have been recovered.

The unemployment rate, meanwhile, improved further in July, falling to 10.2% from 11.1% in June, as the number of unemployed persons fell by 1.4 million. The theme of more Americans being called back to work remained evident in July as the number of people on temporary layoff fell 1.3 million to 9.2 million, while the number of those on permanent layoff was virtually unchanged at 2.9 million.

Despite everything, there are indications that this latest health-induced hurdle too shall pass in time. For instance, over the last several days, infections appear to be slowing again on a trend basis (Chart 2). If sustained, this downward trajectory will eventually help grease the wheels of the reopening process.

At the same time, a new stimulus package that’s being negotiated in Washington is expected to lend another hand to the recovery. Hopes are high for stimulus on several fronts (enhanced unemployment benefits, stimulus checks, aid to small business and state and local governments, along with rent, mortgage and food assistance). But, given large outstanding differences in Congress, it is unclear if an agreement can be achieved in short order. Timing is of the essence to avoid further financial stress and to support the confidence channel.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.