HIGHLIGHTS OF THE WEEK

- Concerns about Turkey drove market volatility this week, but U.S. equity markets managed a rebound.

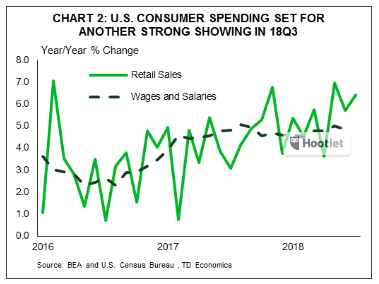

- Strong retail sales and historically-high small business optimism suggest a strong economic expansion in the U.S. this quarter.

- Although concerns eased by week’s end, Turkey is not out of the woods yet. It remains in the early stages of a balance of payments crisis, and is likely to trigger further bouts of market volatility.

Markets Brush Aside Emerging Market Fears For Now

Like Argentina, Turkey is too small in the scope of the global economy to trigger a broader global crisis. Turkey’s economy is responsible for about 1.7% of global annual output (2016 purchasing power parity), a little more than Canada at 1.4%. Contagion risk via trade linkages is low, although Europe is most exposed. Similarly, financial contagion is limited, with Spanish, Italian, and French banks at risk to lose a tiny proportion of foreign loans.

That said, contagion to other economies can still occur through confidence and sentiment channels. That was evident this week with the turmoil in global financial markets that drove a selloff in risk assets and emerging market currencies, and a bid for developed market bonds. Further bouts of volatility are likely as emerging market economies with large imbalances are targeted one-by-one by increasingly discerning investors.

Although concerns eased by week’s end, Turkey is not out of the woods yet. It remains in the early stages of a balance of payments crisis. A sudden stop to capital inflows has occurred, and the next step for Turkey involves spending cuts and an emphasis on boosting exports to help generate foreign currency required to pay for its large external obligations. The medicine will be bitter, but the sooner Turkish authorities follow through with interest rate increases, capital controls, and fiscal spending cuts, the more likely they can mitigate the economic fallout.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.