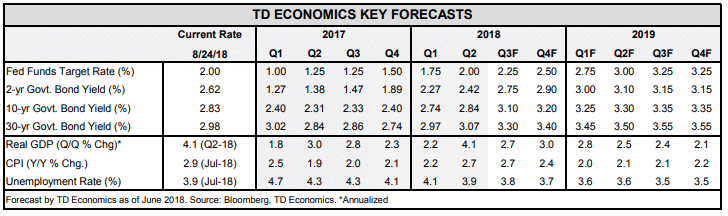

HIGHLIGHTS OF THE WEEK

- Financial markets jitters have eased somewhat this week as concerns about emerging countries have temporarily subsided, helped in part by a lower U.S. dollar.

- Economic data was mixed. U.S. business investment remained upbeat in July, with new orders of capital goods (ex. aircraft) rising 1.4% m/m. Meanwhile, the housing market disappointed yet again in July.

- On the policy front, FOMC meeting minutes and a speech by Chairman Powell noted the recent strength in economic performance and confidence in the outlook, signaling continued gradual interest rate increases.

FOMC Signals Continued Gradual Rate Hikes

Financial markets’ jitters eased somewhat this week as concerns about emerging countries have temporality subsided. This was helped by the lower U.S. dollar, which has reversed some of its recent strength following president Trump’s comments that he was “not thrilled” about the Fed’s interest rate increases.

While the U.S. economy, broadly, is running at full throttle, the housing market has hit a speed bump (see Chart 1). Both new and existing home sales failed to make headway in the first half of the year, and this week’s data suggests that the softness has extended into the third quarter. Existing home sales declined for a fourth consecutive month in July (-0.7% m/m), while sales of new homes slipped by 1.7% m/m, suggesting residential investment could again weigh on GDP growth in Q3.

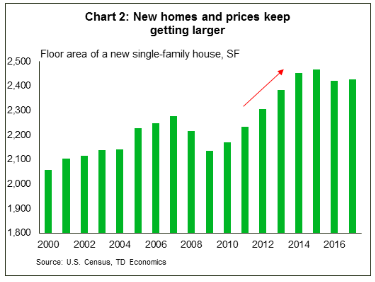

It is hard to square the housing market underperformance amid strength in other sectors of the economy as well as rising employment and incomes. Most commentators chalk tepid sales to low inventory, particularly in the entry-level segment. While new construction has been rising, it has been skewed toward higher end of the market with houses getting progressively larger during the recovery. Square footage of the median house was 13% larger in 2017 than it was back in 2004 (see Chart 2). Rising home prices and mortgage rates, which are up nearly 60 basis points since last year, have also dented affordability. These and other headwinds are likely to persist in the near term, however, but there are also some silver linings: price growth appears to be slowing and housing inventory finally stopped shrinking in July (on a y/y basis), stabilizing for the first time since the end of 2014..

Ksenia Bushmeneva, Economist | 416-308-7392

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.