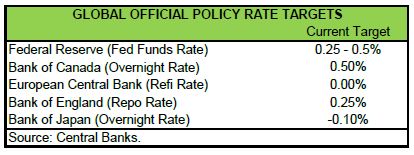

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Economic data this week were supportive of the narrative of ongoing improvement in activity. Despite a slight downward revision to estimated real GDP growth in the second quarter (1.1% from 1.2%), the details showed an upward revision to consumer spending and business investment and a slightly larger drawdown in inventories.

- Janet Yellen’s speech in Jackson Hole noted the improvement, saying at “in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months.”

- With considerable uncertainty around the eventual neutral interest rate, the pace of future rate hikes will be glacial and contingent on ongoing calm in global financial markets.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

THE FAULT IS IN R-STAR

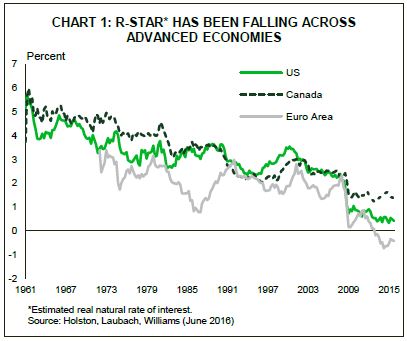

If you have been paying attention to Fed speak over the dog days of summer, you have likely heard talk of the “r-star.” It sounds arcane, but don’t let that fool you. While the concept is theoretical, its implications are real. As the Federal Reserve considers its next steps in normalizing monetary policy, estimates of “r-star” or neutral rate of interest will be a key determining factor.

Stated simply, the neutral rate is defined as the rate of interest at which there is neither upward or downward pressure on inflation. In theory, this rate is determined by the supply of savings relative to the demand for investment. In practical terms, the neutral rate is influenced by things like population growth, aging, and productivity growth.

The important point for investors is that current estimates of the neutral rate are thought to be much lower than in previous cycles. According to a paper co-authored by San Francisco Federal Reserve president John Williams, the current real (inflation-adjusted) neutral rate is somewhere in the neighborhood of 0%. With inflation of 2%, this implies a nominal neutral rate that is also 2%.

A few points bear making. One, there is no guarantee that the current neutral rate will remain the prevailing rate in the future. Shifts in preferences for saving or in opportunities for productive investment can shift the r-star. Unfortunately, estimating the neutral rate is an inherently backward looking process and gives us little indication of its future path. Second, a time varying neutral rate adds another layer of uncertainty to predicting the actual course of monetary policy. One can see this in Federal Open Market Committee (FOMC) participants’ own expectations for the fed funds rate. While the current consensus in terms of the long-run rate appears to be in the neighborhood of 3.0%, it has fallen 80 basis points since reporting began over the last year.

Even more, there appears to be little agreement about when this longer-run rate will prevail. At least one FOMC participant, James Bullard of the St. Louis Federal Reserve, has a base-case

This provides important context for debate currently occurring both within the fed and in financial markets about when the Fed will next raise interest rates. A chorus of Fed speakers have sounded the drum on the likelihood of an imminent rate hike. Janet Yellen, in her speech Friday in Jackson Hole, noted that “in light of the continued solid performance of the labor market and our outlook for economic activity and inflation, I believe the case for an increase in the federal funds rate has strengthened in recent months.”

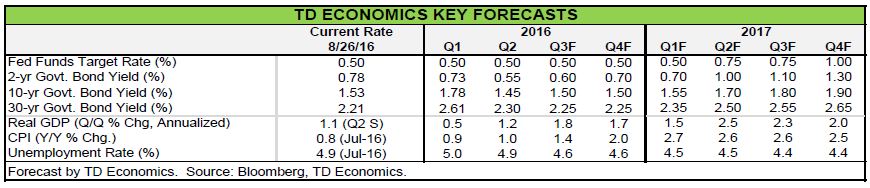

Given the stream of recent economic data, including this week’s revision to second quarter GDP growth, which showed an even higher rate of consumer spending and modestly upgraded inflation, the odds of the Fed raising rates before the end of this year are close to even. Nevertheless, there is little reason to expect the neutral rate to move much from its current low level. This means that the most that can be expected in terms of future rate hikes is one to two per year. And as we’ve seen over the course of this year, it will not take much in terms of global financial volatility to put off even this very modest pace of tightening.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.