FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Market volatility picked up this week after a post-Brexit summer slumber, with moves dominated by speculation on whether we’ve seen the bottom for longer-term global interest rates. Hawkish statements by Fed presidents were trumped later by governor Lael Brainard’s speech, convincing the market that the fed will wait until December for its next rate hike.

- Mixed U.S. economic data this week was consistent with a cautious, patient Fed. Weaker than expected retail sales and industrial production data for August suggested modestly slower growth in 16H2, while stronger inflation data is consistent with absorption of economic slack.

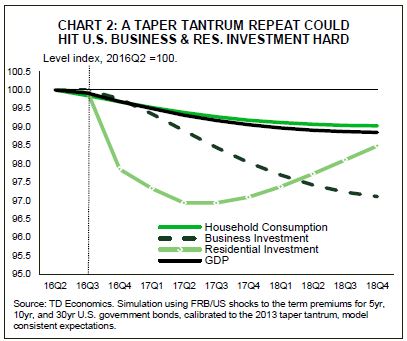

- Global economic data show growth picking up in the second half of the year, but financial fragilities remain at the forefront. Speculation about BoJ policy added to the pressure this week, spurring a sell-off in advanced economy bonds. A repeat of the 2013 taper tantrum episode would have serious negative repercussions on the U.S. outlook.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

VOLATILITY RETUNS IN SEPTEMBER

In the lead-up to next week’s FOMC meeting, market action this week was dominated not only by speculation of whether the Fed would raise rates, but also concerns that maybe, just maybe,

The global data flow this week was generally positive, confirming that demand is heating up in the second half of this year. UK retail sales for August failed to fully reverse the strength in July, giving further credence to the idea that the UK economy post-Brexit is generally evolving in line with the Bank of England’s August forecast. Furthermore, Chinese data for August confirm that growth will remain close to 7.0% (annualized q/q) in the third quarter, driven by strength in the services sector.

However, underneath this thin veneer of global stability

As we show in Chart 2, a shock to U.S. term premiums similar in magnitude to that observed in 2013 would be detrimental to the outlook for the U.S. economy. Business and residential investment would be hardest hit, falling close to 3% and 2.5% respectively below our baseline by the end of 2018. Overall, U.S. economic output would be about 1.2% weaker.

All told, with signs that excess slack continues to be absorbed in the U.S. economy and global demand is recovering, conditions are ripe for a fed rate hike. However, the risks remain titled to the downside, implying that a cautious Fed will likely defer a rate hike until December.

Fotios Raptis, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.