FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

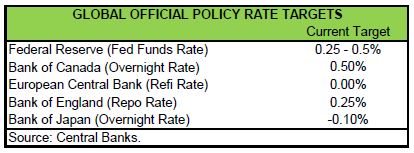

- The Bank of Japan announced two new policy measures this week, aiming to target the interest rate on the longer-end of the curve at zero, and pledging to let inflation overshoot the target – effectively committing to be slightly irresponsible. Still, a lack of an interest rate cut fanned the view that the BoJ may be running out of ammunition, which together with fears that these moves are too late, has thrown into question the efficacy of the new measures.

- The Fed also left its policy rate unchanged on Wednesday, albeit only “for the time being.” The case for a rate hike has strengthened, according to the Fed, with three members wanting to lift rates this week-exemplified by a rare triple dissent. The Fed has all but set itself up for a hike later this year, with most members remaining optimistic for the economic outlook. Having said that, future rate hikes are likely to be more gradual, with the Fed’s own projections toned down alongside potential growth estimates.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

FED STANDS PAT… FOR THE TIME BEING

This week has been rather an exhilarating one in financial markets. Alongside some weak data on domestic housing activity, investors were treated to two major central bank announcements

The Bank of Japan surprised many investors by adopting a couple of policy measures that were previously thought of as too radical by the bank. The first, referred to as yield curve control, aims to target the interest rate on the longerend of the curve at zero. The BoJ has essentially announced it will buy any 10-year JGBs should their price fall to that level. Secondly, Governor Kuroda pledged to let inflation overshoot the target – effectively committing to be slightly irresponsible. The BoJ also tweaked its QE allocation, aiming to buy more short-term debt to help steepen the yield curve and reweighing ETF purchases towards the domesticoriented Topix index away from the export-heavy Nikkei.

The BoJ did not lower interest rates, merely suggesting that such a move remains a “possible option for additional easing.” Lack of a cut fanned the view that the BoJ may be running out of ammo, which together with fears that these moves are too late, has thrown into question the efficacy of the new measures. The Bank has failed to fend off the deflationary mindset for years, with the pledge to overshoot only helpful if the target can be reached in the first place.

Across the Pacific, the Fed too, left its policy rate unchanged on Wednesday.

As such, the Fed has all but set itself up for a hike later this year. Fourteen of the seventeen officials now expect a rate hike later this year. Moreover, three of the ten voting members wanted a hike this week – a rare dissent that highlights divisions on the Committee. The Fed has made significant progress towards its dual objectives, particularly on the jobs front, with most believing the U.S. labor market is nearing full-employment. At the same time, while inflation remains below target suggesting patience, lags in monetary policy and fears that the fully utilized resources will soon begin to manifest on prices level appear to be swaying more members to want to get ahead of the curve.

All this suggests that the Fed will move sooner, but proceed more gradually. Such a scenario is corroborated by Fed members’ own projections, which have been revised lower and suggest a shallower path for future rates. Given the U.S. Presidential elections, we expect the Fed will opt to wait until December to raise rates. This should be a short-enough delay to keep the hawks at bay, while providing enough time to gather evidence of U.S. economic resilience. Having said that, such an outcome is not assured, with risks ranging from global imbalances to U.S. elections far from immaterial.

Michael Dolega, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.