FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Concerns over German banks and a surprise production cut announcement by OPEC provided some volatility to financial markets this week.

- Economic data was mixed this week. Second quarter real GDP was revised up to 1.4% (from 1.1%), and August goods exports beat-expectations. This was offset by weaker-than-anticipated consumer spending data in the month, which declined 0.1%.

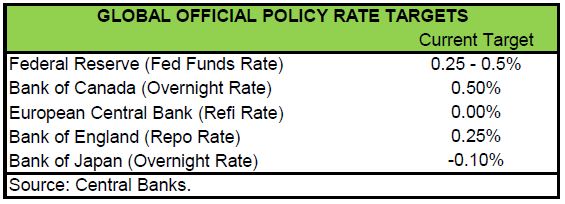

- While the composition has shifted slightly toward foreign demand and away from domestic demand, the economy continues to track real GDP growth close to 3.0% in the third quarter, enough for the Federal Reserve to remain on course for a December rate hike. A key data point to watch on this front is next week’s payroll report for September, where we expect a gain of 160k jobs – slower than earlier in the recovery, but still consistent with ongoing labor market improvement.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

VOLATILITY TO CONTINUE

Concerns over German banks and a surprise production cut announcement by OPEC provided some volatility to financial markets this week. Equity markets were up following the OPEC

The see-saw action is likely to continue as financial markets digest a number of key event risks over the next several months including the U.S. election, another OPEC meeting in November, an Italian constitutional referendum, and last but not least, a potential rate hike by the Federal Reserve.

OPEC’s extraordinary meeting was light on details, but telegraphed its intent to cut production to a target range between 32.5 and 33 million barrels a day. The WTI benchmark price rose an initial 5% from $44 to over $47 in reaction to the cut and has moved above $48 per barrel this morning. This is likely to be the extent of the impact, however, as continued oversupply should limit any further price gains. We expect prices to remain in the US$40-50 per barrel range in the near term, before gradually trending above US$50 per barrel in 2017 as the market moves into a more balanced position.

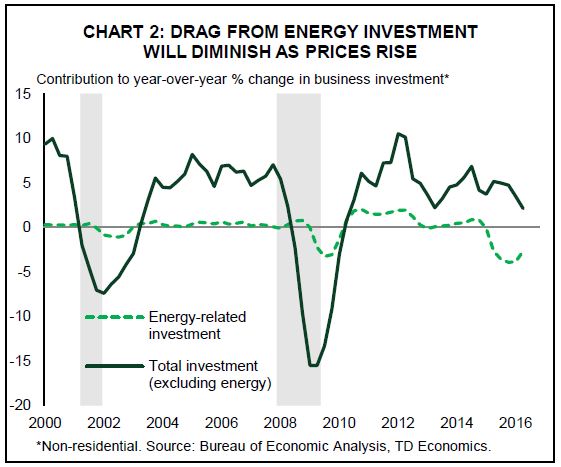

Still, slowly rising oil prices should provide some reprieve to shale producers and limit any further reductions in oil-related investment. This is welcome following six straight quarters in which declining oil exploration has cut an average of 0.3 percentage points (annualized) from quarterly real GDP growth. Unfortunately, overall business investment will continue to be a weak spot for the American economy in the third quarter, as telegraphed this week by a 0.4% decline in core durable goods shipments. The good news is that even as shipments fell, new orders rose, suggesting

that investment will pick up in the months ahead.

Other economic data was mixed this week. Second quarter real GDP was revised up to 1.4% (from 1.1%), largely on a smaller declines in business investment and stronger export growth. Export momentum continued into the third quarter with a 1.5% increase in August. Combined with a smaller gain in imports, net exports should contribute positively to third quarter growth.

These positive developments were offset by a downward revision to consumer spending (to 4.3% from 4.4%) in the second quarter and a disappointing outturn for monthly spending in August. Led by a pullback in durable goods, real personal consumption expenditures declined 0.1% on the month. As a result, the tracking for consumer spending growth has fallen to 2.7% (from 3.0% in our recent QEF). All told, while GDP is still tracking growth of slightly under 3.0%, the composition suggests a bit more foreign demand and a bit less domestic demand. As long as this progress is maintained, the Federal Reserve will remain on track to raise interest rates. With a rate hike a week before the November election unlikely, a December hike still appears the most likely scenario. A

key data point to watch on this front is next week’s payroll report for September, where we expect a gain of 160k jobs– slower than earlier in the recovery, but still consistent with ongoing labor market improvement.

James Marple, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.