FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

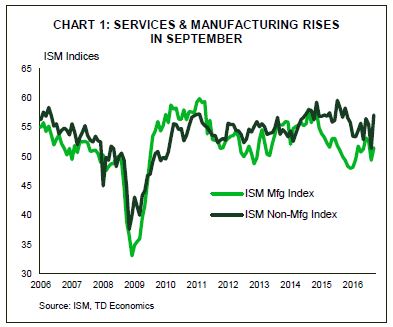

- While attention is focused on Hurricane Matthew, at least there was some good news from the U.S. economy. Both ISM sentiment indices pointed to greater confidence in September for manufacturing and services.

- A solid employment report added to the good news, with 156K workers added to payrolls in September. The details were also good, with the slight uptick in the unemployment rate from 4.9% to 5.0% due to a growing labor force, rather than job losses.

- Unfortunately, things weren’t so rosy across the pond. Recent statements from leaders in the UK and France reminded markets that “Brexit means Brexit”, which took the pound sharply lower on the week.

[su_row][su_column size=”1/2″]

[/su_column]

[su_column size=”1/2″]

[/su_column][/su_row]

AMERICANS GO BACK TO WORK IN SEPTEMBER

Many in the U.S. are more focused on potential damage being caused by Hurricane Matthew bearing down on the south this week, but the news for the economy was much sunnier. The overall

For the U.S. economy, the good news started with the ISM Manufacturing Index, which provided some reassurance industry is weathering the strong dollar and weak global growth. The index moved back up above 50 (see Chart 1), indicating expansion. It was followed with a jump up in the services ISM, also pointing to greater confidence on the services side of the economy. One of the more tangible measures of consumer confidence is auto sales, given the big ticket nature of the purchase, and sales in September improved. Solid September sales rounded out the strongest quarter since last year. This helps underpin our recent forecast that healthy consumer spending in Q3 was likely driven by durable goods purchases.

The September jobs report provided further evidence that robust consumer spending is well-supported by continued job gains. 156K new jobs were added to payrolls in September, roughly as we expected. Normally we wouldn’t cheer an uptick in the unemployment rate (from 4.9% to 5.0%), but in this case it was due to an increase in labor force participation, which is positive. The low level of labor force participation since the recession has been a

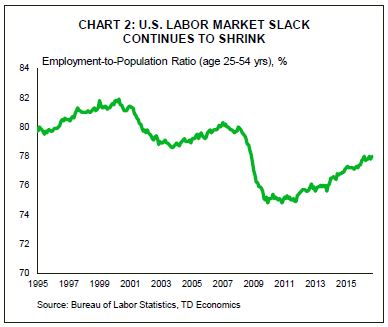

Zeroing in on the core working age employment rate (age 25 to 54), which removes the downward influence of population aging on the rate, the amount of “slack” in the labor market has made notable progress (see Chart 2). The stronger labor market is clearly drawing new, or previously discouraged, workers into the job market. This will please the Fed, as Chair Yellen has referred to slack remaining in the labor market.

The combination of higher oil prices and better economic growth signals also took market-based measures of inflation expectations (such as the 5-yr-5-yr breakeven rate) to their highest readings since May. This will also be welcomed by the Fed, which wants to see more evidence of inflation before raising rates again. Add it all up, and our case for a December rate hike has strengthened over the past week.

It wasn’t so long ago that the Bank of England was expected to be the next major central bank to raise interest rates. But the Brexit vote put a stop to that. Sentiment on the UK economy weakened even further this week as financial markets give up hope on a “soft” Brexit. Unsurprisingly, without preferential access to the UK’s largest export market the outlook for the UK dims. This has further dampened market sentiment on the pound, which now sits at its lowest level since 1985.

Leslie Preston, Senior Economist

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.