Financial News Highlights

- Fed Chair Jay Powell’s hawkish remarks at the annual Jackson Hole conference did not sit well with equity markets.

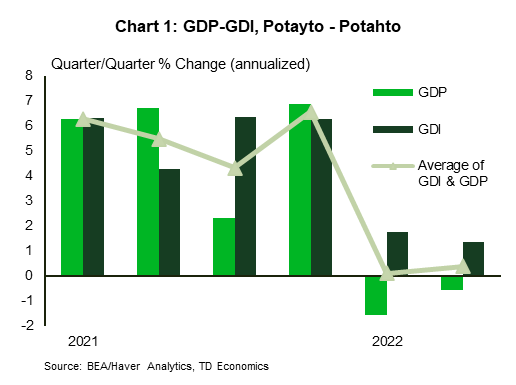

- The second estimate of Q2 GDP data showed that the economy contracted slightly less, and that GDI grew modestly. looking at an average of the two measures shows that the U.S. economy grew only slightly in the first half of the year.

- President Biden announced details on a much-anticipated student debt forgiveness plan that will forgive up to $20,000 in federal student debt per borrower.

- A reduction in student debt will be stimulative for people receiving the relief, and could add more fire to current inflationary pressures, making the Fed’s job that much more difficult.

U.S. – Powell Stands Firm on Higher Rates

It was a full week for economic data, but the most anticipated event for markets was the Fed Chair’s speech at the annual Jackson Hole conference on Friday in financial news. Equity markets didn’t like what they heard. Powell’s hawkish remarks that the Fed remains committed to fight inflation and is likely to keep rates high for an extended period did not sit well with investors, and stocks fell on the remarks. The yield on the 2-Year Treasury was up slightly after the speech, continuing a recent trend as markets expect a bit more monetary tightening over the next two years.

It was a full week for economic data, but the most anticipated event for markets was the Fed Chair’s speech at the annual Jackson Hole conference on Friday in financial news. Equity markets didn’t like what they heard. Powell’s hawkish remarks that the Fed remains committed to fight inflation and is likely to keep rates high for an extended period did not sit well with investors, and stocks fell on the remarks. The yield on the 2-Year Treasury was up slightly after the speech, continuing a recent trend as markets expect a bit more monetary tightening over the next two years.

Longer-term bond yields remain lower than the 2-Year as markets expect an economic slowing and future rate cuts by the Fed. It is understandable that investors are worried about a recession, when the second estimate for GDP growth in Q2, was revised up only slightly and still contracted by 0.6% annualized. This release was more highly anticipated than usual because it included another measure of national output – Gross Domestic Income (GDI). GDI measures output based on income in the economy – summing wages, profits, interest payments and investments. Whereas GDP is defined as the value of final goods and services on the production side. In theory they should be similar, but there usually is some deviation due to being measured from different data sources.

Some economists argue that GDI is the better measure – but it is released later by the BEA, and so usually gets less attention. Early estimates of GDI better captured the downturn in the 2007-09 recession. The compromise is that an average between the two measures likely captures momentum in the economy best. In the first half of 2022, GDP estimates suggested the economy contracted, while GDI showed the economy grew at 1.6% on average through Q1-Q2 (Chart 1). The average of the two measures shows the economy stalled in the first half of the year, so to some extent it feels like a potayto-potahto situation – either way you slice it, the U.S. economy is on a dramatically slower growth trajectory in 2022 in the face of high inflation, rising interest rates and less fiscal stimulus.

As for momentum in the second half of the year, consumer spending data for July showed that nominal spending continued to lose momentum. But, due to weaker inflation pressures, the real spending slowdown is somewhat less than we expected a few weeks ago. Real consumer spending is tracking around 1.5-2% annualized in the third quarter, which is roughly the same pace averaged over the first half of the year in financial news. This suggests the consumer is proving quite resilient to all the onslaughts against their purchasing power.

As for momentum in the second half of the year, consumer spending data for July showed that nominal spending continued to lose momentum. But, due to weaker inflation pressures, the real spending slowdown is somewhat less than we expected a few weeks ago. Real consumer spending is tracking around 1.5-2% annualized in the third quarter, which is roughly the same pace averaged over the first half of the year in financial news. This suggests the consumer is proving quite resilient to all the onslaughts against their purchasing power.

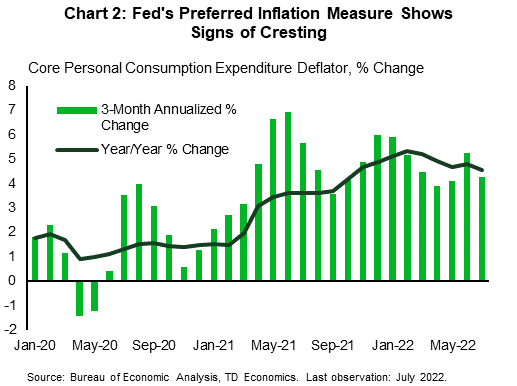

Inflation, as measured by the core PCE deflator, also cooled a bit in July. Looking at it on a year-on-year basis, core inflation has cooled to 4.6%, and ran at a 4.3% annualized pace over the past three months (Chart 2). We aren’t saying that inflation pressures have been vanquished, but it is encouraging they are moving in the right direction. Given the false dawn we had last year, where inflation pressures originally cooled, only to quickly heat up again, Chair Powell is right to point out that the Fed needs to see more convincing evidence before easing up on rate hikes.

Leslie Preston, Senior Economist | 416-983-7053

U.S. Students Get Up to $20,000 in Student Debt Erased

President Biden announced a much-anticipated executive action to reduce the burden of federal student debt in financial news. At the time of writing, the White House hasn’t provided cost estimates, or all the details, but according to the Committee for a Responsible Federal Budget, the plan will cost roughly $500 billion dollars over the next 10 years.

President Biden announced a much-anticipated executive action to reduce the burden of federal student debt in financial news. At the time of writing, the White House hasn’t provided cost estimates, or all the details, but according to the Committee for a Responsible Federal Budget, the plan will cost roughly $500 billion dollars over the next 10 years.

Under the plan, $10,000 in federal student loan debt will be forgiven for borrowers making under $125,000 (or $250,000 for couples). Approximately 40 million borrowers would be eligible for this amount. In addition, up to $20,000 will be forgiven for the 27 million recipients of Pell Grants – a specific program for students in financial need. It’s estimated that more than a third of the total $1.6 trillion in student debt will be forgiven.

The plan also modifies existing income-driven repayments by reducing future monthly payments for lower-and middle-income borrowers. Payments will be reduced from 10% to 5% percent of discretionary income, and forgives loan balances of $12,000 or less after 10 years.

Furthermore, borrowers who are employed by non-profits, the military, or government may be eligible to have all their student loans forgiven through the Public Service Loan Forgiveness program. The pandemic moratorium on federal student loan payments will also be extended through December 31st, saving roughly $20 billion in debt payments.

The announcement puts an end to a debate that has been around since at least the Occupy Wall Street protests a decade ago. The proponents of forgiveness argue it would stop the racial wealth gap from growing and help borrowers turn regular earnings into longer-lasting wealth. Indeed, African American college graduates hold disproportionally large student debt balances in comparison to peers (Chart 1). Those against forgiveness point out that student debt is disproportionately held by more affluent families, and that it will stimulate economic activity at the time when inflation is already running hot.

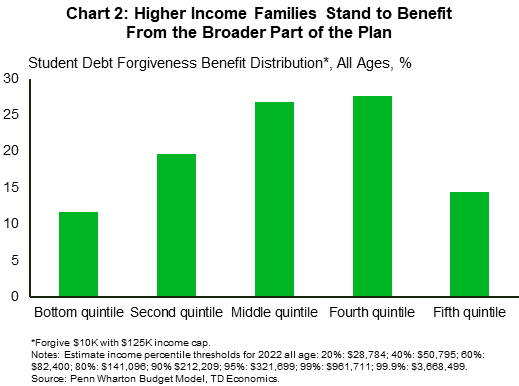

The debate is hot but ultimately the additional forgiveness of $20,000 for Pell grant recipients and modifications to income-driven repayment programs makes the plan more targeted towards lower-income Americans, helping the administration achieve progressive goals. According to White House’s estimates, 87% of the relief will go to lower-income families earning less than $75,000. However, some portion of higher income families stand to benefit, given that the income threshold set at $125,000 is well above the median American income (Chart 2).

In terms of the economic impact, a reduction in student debt will be mildly stimulative, though the average borrower can expect to have their annual payment reduced by $1,000. While there’s still uncertainty over both the timing and implementation of the program, preliminary estimates suggest that the impact to economic growth will be relatively small compared to its cost – with only a tenth of the dollar amount forgiven expected to flow back into the economy. Still, more economic stimulus at time when inflation is already running at multidecade highs will make the Fed’s job that much harder to regain price stability over the coming years.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.