Financial News Highlights

- A strong week for economic data as the ISM manufacturing index and the payrolls report surprised to the upside.

- The details of both reports showed improvements on the supply-side of the economy as falling manufacturer input prices and a strong improvement in the labor force shined through.

- The Fed still has its hands full taming inflation, but supply-side improvements could make the job much easier.

U.S. –

Good News on Aggregate Supply

Markets continued to sell off this week as better than expected data dimmed the hopes of a 50-basis point hike by the Fed at its upcoming September meeting in financial news. However, there were some reassuring signals in the ISM manufacturing report and the household employment survey that the supply-side of the economy continues to improve and may help moderate inflation. The Fed will continue its hiking cycle, but the supply-side improvements might just make the job of taming inflation a bit easier.

Markets continued to sell off this week as better than expected data dimmed the hopes of a 50-basis point hike by the Fed at its upcoming September meeting in financial news. However, there were some reassuring signals in the ISM manufacturing report and the household employment survey that the supply-side of the economy continues to improve and may help moderate inflation. The Fed will continue its hiking cycle, but the supply-side improvements might just make the job of taming inflation a bit easier.

Tuesday’s solid job openings data from the JOLTS survey grabbed headlines. Private openings in July were north of 10 million. Though sky high job openings have become the norm, they are remarkable relative to history and represent the scale of the problem the Fed is looking to solve. To tame inflation, officials are hoping to lower the rate of job openings, without meaningfully raising the unemployment rate. There is little historical precedent for this, but there is also little modern historical precedent for what has transpired in the economy over the past two years. Nonetheless, with job openings still high, the labor market is signaling that employment demand remained robust in July despite rising interest rates.

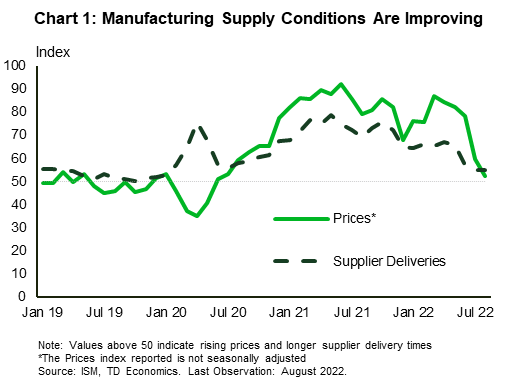

The good economic news continued yesterday as the ISM manufacturing index surprised to the upside in August, registering a healthy 52.8 print. Growth and production were notably slower than earlier in the recovery, but this was to be expected as the economy continues to operate in excess demand territory. The details in the report were also strong. New orders flipped back to growth and employment was up for the month. For the Fed, there was good news on supply chains as the supplier delivery index was unchanged and input price growth eased to its lowest rate since the summer of 2020 [Chart 1].

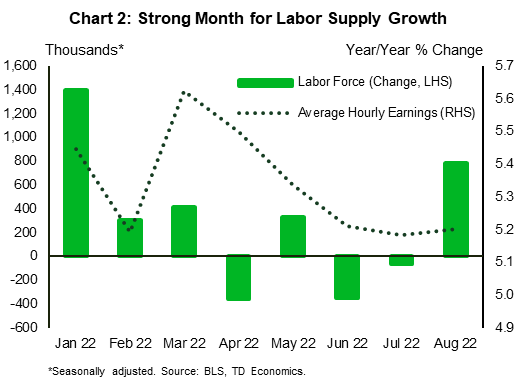

All of this was a buildup to today’s employment report. Consensus expectations were for nearly 300k new jobs, a print that would register as “good” during any expansion, let alone one that has featured so little bounce-back in the participation rate. Well, the data came in slightly better than expected, with payrolls adding 312k jobs, but it was the household report that had some positive elements. August showed that there was finally a large movement of people back into the labor force, 786k to be exact [Chart 2]. This helped lift the participation rate 0.3 percentage points, to 62.4% and brought some much-needed supply to the labor market. As the labor force expanded faster than employment, the unemployment rate rose to 3.7%. With just a bit more labor supply, average weekly wages moderated to 0.3% month-on-month, from 0.5% the month prior.

All of this was a buildup to today’s employment report. Consensus expectations were for nearly 300k new jobs, a print that would register as “good” during any expansion, let alone one that has featured so little bounce-back in the participation rate. Well, the data came in slightly better than expected, with payrolls adding 312k jobs, but it was the household report that had some positive elements. August showed that there was finally a large movement of people back into the labor force, 786k to be exact [Chart 2]. This helped lift the participation rate 0.3 percentage points, to 62.4% and brought some much-needed supply to the labor market. As the labor force expanded faster than employment, the unemployment rate rose to 3.7%. With just a bit more labor supply, average weekly wages moderated to 0.3% month-on-month, from 0.5% the month prior.

The Fed will see this report as good news. The drum-tight labor market is a key factor in setting wage expectations, and with more workers coming in off the sidelines, it means just a bit less wage pressure in further financial news. That said, labor markets remain tight as wage growth is still at 5.2% year-on-year, and inflation is still persistently high. The Fed will continue to raise rates to fight inflation, but this week’s data suggest that some of the supply-side factors behind current price growth are finally starting to abate.

Andrew Hencic, Senior Economist | 416-944-5307

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.