Financial News Highlights

- The ISM Services index expanded at the fastest pace in four months with demand components rising and supply side challenges normalizing.

- The Fed’s Beige book pointed to a further softening in demand, while also suggesting that labor markets remained tight.

- A hot labor market is contributing to the Fed’s hard line on inflation emphasized in speeches this week. This solidified market expectations for a three-quarter hike in September.

U.S. – Fedspeak Solidifies Bets for Supersized Hike

The first post-Labor-Day week was scant on economic data, but markets had plenty of remarks from FOMC members to digest in financial news. Fed speakers’ hawkish message led Treasury yields higher, with the 2-Year yield up 12 basis points (bps) and the 10-Year yield up 10 bps on the week, at time of writing. The economic data was largely second tier sentiment surveys, which sent some conflicting signals.

The first post-Labor-Day week was scant on economic data, but markets had plenty of remarks from FOMC members to digest in financial news. Fed speakers’ hawkish message led Treasury yields higher, with the 2-Year yield up 12 basis points (bps) and the 10-Year yield up 10 bps on the week, at time of writing. The economic data was largely second tier sentiment surveys, which sent some conflicting signals.

The ISM Services index rose in August, expanding at the fastest pace in four months. The underlying measures remained on the right track. The demand components – such as business activity and new orders – reached above 60 for the first time since December and March, respectively. Meanwhile, supply-side challenges continue to normalize with employment subindex moving into the expansionary territory, supplier deliveries times returning to their pre-pandemic average, and prices paid component easing.

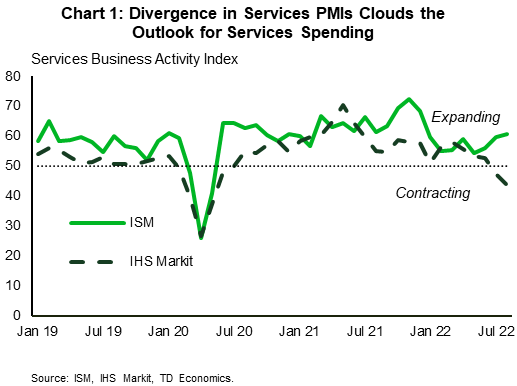

Yet, the reading came as a surprise as consensus was pricing a moderation, and the other services flash indicator – the IHS Markit PMI – contracted in August. Demand components were especially contrasting, as the ISM index suggested strengthening while the IHS Markit pointed to a looming demand destruction (Chart 1). The differences in methodology explain the divergence in the signals: the ISM index includes a broader range of industries (including construction and mining) and reflects business conditions of its members who tend to be larger and more established companies. The IHS measure therefore better reflects the sentiment of small- and medium-sized enterprises, but we find that the ISM index has stronger historical correlations with services spending.

While this divergence clouds the outlook, we expect the truth to lie somewhere in the middle, with current economic activity remaining unchanged. This sentiment was echoed in the Fed’s Beige book that gathers anecdotal information on current economic conditions through July and August across Federal Reserve Bank districts. The report characterizes consumer spending as “steady” and points to expectations for further softening of demand over the next six to twelve months in further financial news. On the other hand, respondents indicated that labor market conditions remained tight, but also pointed to a slower pace of wage increases and moderating salary expectations.

While this divergence clouds the outlook, we expect the truth to lie somewhere in the middle, with current economic activity remaining unchanged. This sentiment was echoed in the Fed’s Beige book that gathers anecdotal information on current economic conditions through July and August across Federal Reserve Bank districts. The report characterizes consumer spending as “steady” and points to expectations for further softening of demand over the next six to twelve months in further financial news. On the other hand, respondents indicated that labor market conditions remained tight, but also pointed to a slower pace of wage increases and moderating salary expectations.

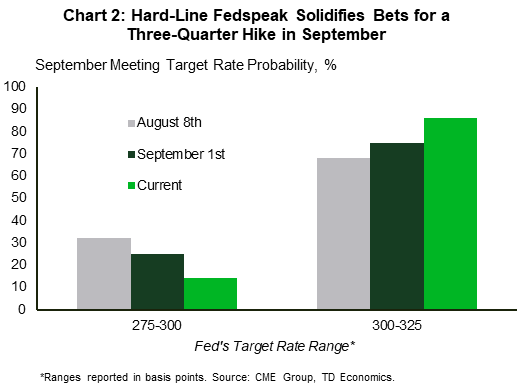

The tightness of labor market is a big part of why the Fed takes a hardline inflation fighting stance. FOMC speakers took every opportunity to reinforce their unanimity on this front ahead of the central bank’s black-out period prior to its September 21st rate decision. Chair Powell was very explicit by stating that the Committee wants to soften growth enough to “cause the labor market to get back into better balance, and then that will bring wages back down to levels that are more consistent with 2% inflation over time.” Investors heard it loud and clear with the federal funds futures markets now have greater conviction that the Fed will hike 75 basis to 3.25% (Chart 2). Moreover, the market appears less convinced that there will be rate cuts next year, buying into the Vice Chair Brainard’s “we are in this for as long as it takes to get inflation down” mantra.

Maria Solovieva, CFA, Economist | 416-380-1195

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.