Financial News Highlights

- CPI inflation surprised to the upside in August, rising 0.1% m/m. The core measure also recorded a sizeable 0.6% m/m gain, as both goods and service categories accelerated on the month.

- Financial markets have now fully priced a 75-basis point hike from the Fed next week and are anticipating the Fed funds rate reaches 4% by year-end.

- A tentative agreement between U.S. rail companies and the unions representing rail workers was reached on Thursday, avoiding what could have been another crippling blow to U.S. supply chains.

Full Steam Ahead for the FOMC

Hopes that the Federal Reserve can still engineer a soft landing were tested again this week in financial news. Consumer Price Index (CPI) data for August showed inflation was far hotter than expected, leading to a sharp repricing of market expectations on the future path of rate hikes. Following the release, market participants were quick to fully price a 75-basis point move from the Federal Reserve next week, and now expect the Fed funds rate to reach 4% by year-end. The pull forward in rate hike expectations triggered a sharp sell-off in U.S. equities, with the S&P 500 suffering its worst day of the year – falling by over 4%. Equities dipped a bit further through the remainder of the week and are down 5.5% at the time of writing.

Hopes that the Federal Reserve can still engineer a soft landing were tested again this week in financial news. Consumer Price Index (CPI) data for August showed inflation was far hotter than expected, leading to a sharp repricing of market expectations on the future path of rate hikes. Following the release, market participants were quick to fully price a 75-basis point move from the Federal Reserve next week, and now expect the Fed funds rate to reach 4% by year-end. The pull forward in rate hike expectations triggered a sharp sell-off in U.S. equities, with the S&P 500 suffering its worst day of the year – falling by over 4%. Equities dipped a bit further through the remainder of the week and are down 5.5% at the time of writing.

In terms of the actual CPI figures, headline inflation rose 0.1% month-on-month (m/m), a few ticks above the consensus forecast. More worrying, was the 0.6% m/m increase in core inflation – a sharp acceleration from July’s 0.3% m/m gain. While some persistence in price growth across service categories such as shelter and healthcare was expected, the August data showed far more breadth and strength across nearly all goods and service categories.

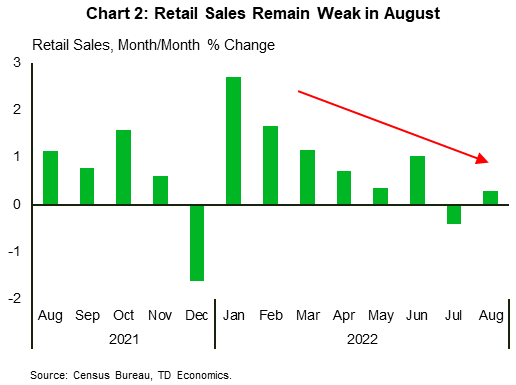

While we’re hesitant to put too much stock in one month of data, the re-acceleration in goods prices is somewhat concerning. Despite demand for consumer goods cooling more recently, goods inflation has shown considerable staying power. This was reaffirmed later in the week where August retail sales data showed only a modest gain of 0.3% m/m (Chart 1). The control group of sales was even weaker, recording a flat reading on the month.

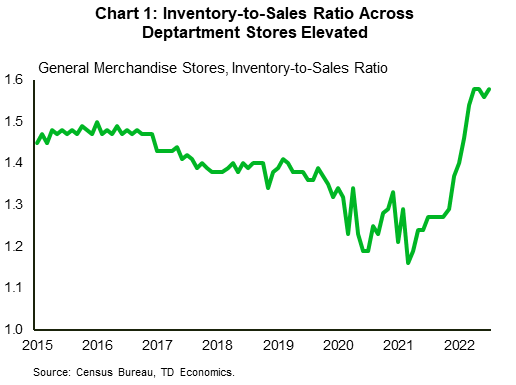

The continued gains in goods prices are even more perplexing when we consider the fact that not only is demand weakening, but inventory levels are also starting to look toppish. Inventory-to-sales ratios across department stores are now well above pre-pandemic levels – suggesting we should be seeing some disinflationary pressure (Chart 2). Other oddities are also starting to emerge across used vehicle prices. The Manheim Used Vehicle Price Index – a measure that captures dealer purchase prices – has fallen by over 10% this year, yet the CPI measure of used vehicle prices has declined by only 1.5%. This suggests that lower costs are not being passed onto consumers, and retailers are instead maintaining wider margins. Over the near-term, this is not necessarily problematic. But if left unchecked, it can start to sow the seeds of more engrained inflationary pressures. Fortunately, that hasn’t happened yet. According to data released by the New York Federal Reserve, both one-and-three-year inflation expectations have continued to move lower, with August readings falling to 5.8% (from 6.2%) and 2.8% (from 3.2%), respectively.

The continued gains in goods prices are even more perplexing when we consider the fact that not only is demand weakening, but inventory levels are also starting to look toppish. Inventory-to-sales ratios across department stores are now well above pre-pandemic levels – suggesting we should be seeing some disinflationary pressure (Chart 2). Other oddities are also starting to emerge across used vehicle prices. The Manheim Used Vehicle Price Index – a measure that captures dealer purchase prices – has fallen by over 10% this year, yet the CPI measure of used vehicle prices has declined by only 1.5%. This suggests that lower costs are not being passed onto consumers, and retailers are instead maintaining wider margins. Over the near-term, this is not necessarily problematic. But if left unchecked, it can start to sow the seeds of more engrained inflationary pressures. Fortunately, that hasn’t happened yet. According to data released by the New York Federal Reserve, both one-and-three-year inflation expectations have continued to move lower, with August readings falling to 5.8% (from 6.2%) and 2.8% (from 3.2%), respectively.

One piece of good news emerged this week, with a tentative agreement reached between U.S. rail companies and the unions representing the rail workers in further financial news. The labor deal averts what would have been another crippling blow to U.S. supply chains, and almost certainly lead to more near-term pressures on inflation. FOMC officials will likely breathe a sigh of relief, as the focus can remain squarely on what will still be a challenging task; threading the needle of lowering inflation while trying to avoid a recession.

Thomas Feltmate, Director & Senior Economist | 416-944-5730

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.