Financial News Highlights

- The Federal Reserve raised interest rates by 75bps for the third consecutive meeting, bringing the federal funds rate to its highest level in 14 years.

- FOMC Chair Powell reiterated his Jackson Hole speech, stating that the Fed is willing to tolerate slower growth and higher unemployment to bring inflation back to its 2% target.

- Interest rate sensitive sectors continue to feel the effects of past rate hikes, with existing home sales down 0.4% (m/m) in August, marking the seventh consecutive month of declines.

The FOMC Aims High

The last days of summer 2022 were centered around the FOMC meeting which ended Wednesday with another 75bps hike, bringing the federal funds rate to its highest level in 14 years in financial news. The announcement was largely expected by markets after last week’s CPI print came in hotter than expected, with core CPI rising to 0.6% month-over-month (m/m). However, the Fed’s updated projections underlined a narrative that was more hawkish than what markets had been expecting, resulting in a volatile reaction from equity and bond markets. The S&P 500 ended the day down by 1.7% and the two-year treasury yield, which briefly rose above 4.1%, closed back at its pre-meeting level of 4%. Further digestion of the decision has seen the two-year yield rise to 4.2% and the S&P 500 retreat further, ending the week down 4.1% as of the time of writing.

The last days of summer 2022 were centered around the FOMC meeting which ended Wednesday with another 75bps hike, bringing the federal funds rate to its highest level in 14 years in financial news. The announcement was largely expected by markets after last week’s CPI print came in hotter than expected, with core CPI rising to 0.6% month-over-month (m/m). However, the Fed’s updated projections underlined a narrative that was more hawkish than what markets had been expecting, resulting in a volatile reaction from equity and bond markets. The S&P 500 ended the day down by 1.7% and the two-year treasury yield, which briefly rose above 4.1%, closed back at its pre-meeting level of 4%. Further digestion of the decision has seen the two-year yield rise to 4.2% and the S&P 500 retreat further, ending the week down 4.1% as of the time of writing.

Chair Powell used his press conference to reiterate his Jackson Hole speech, emphasizing that the Fed would not shy away from its fight to bring inflation back to its 2% target. Powell noted that a restrictive policy stance would likely be required for some time and that this would likely result in a sustained period of below trend growth and softer labor market conditions. Progress on the inflation front has been mixed so far with headline inflation showing early signs of peaking (largely due to falling gas prices), but core inflation has remained stubbornly high which has prompted the Fed to hold the line on its aggressive policy stance.

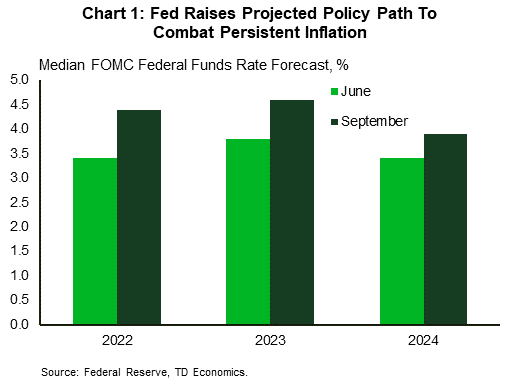

According to the updated Fed projections, the median estimate for the federal funds rate (FFR) is now expected to reach 4.4% by year-end, a full percentage point above their previous estimate in June (Chart 1). FOMC members expect that further rate increases will be required in 2023, with the median projection for the terminal rate reaching 4.6%. This represents roughly 150bps of further rate increases from the current level of 3 – 3.25.

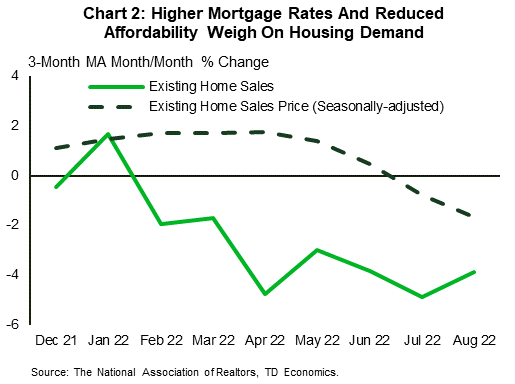

Elsewhere this week, the interest rate sensitive housing sector continued to show further signs of softening. Existing home sales declined by 0.4% m/m in August, marking its seventh consecutive month of declines. Seasonally adjusted median home prices also dipped deeper into negative territory, falling for the three straight months (Chart 2). Reduced affordability continues to act a headwind on consumer demand for housing, and with mortgage rates now well above 6%, that headwind is turning into a gale. Higher rates are not only affecting sales, but also residential construction. While housing starts rebounded in August (rising 12% m/m to 1.58M units), the 3-month moving average of year-over-year changes is still down 5.4%. Moreover, a pullback in August housing permits suggests more weakness in the months ahead. This lines up with recent readings of builder sentiment, which has now fallen for nine consecutive months and currently sits at a 28-month low.

Elsewhere this week, the interest rate sensitive housing sector continued to show further signs of softening. Existing home sales declined by 0.4% m/m in August, marking its seventh consecutive month of declines. Seasonally adjusted median home prices also dipped deeper into negative territory, falling for the three straight months (Chart 2). Reduced affordability continues to act a headwind on consumer demand for housing, and with mortgage rates now well above 6%, that headwind is turning into a gale. Higher rates are not only affecting sales, but also residential construction. While housing starts rebounded in August (rising 12% m/m to 1.58M units), the 3-month moving average of year-over-year changes is still down 5.4%. Moreover, a pullback in August housing permits suggests more weakness in the months ahead. This lines up with recent readings of builder sentiment, which has now fallen for nine consecutive months and currently sits at a 28-month low.

None of this will sway the Federal Reserve to lift its foot off the pedal as they continue to drive interest rates higher to bring down inflation. With the FOMC charting a course that nearly inverts the 2007/2008 run-down in the policy rate, the current and expected future path of monetary policy will continue to act as an increasing weight on the economy moving forward in financial news.

Andrew Foran, Economist | Andrew.Foran@td.com

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.