Financial News Highlights

- The last jobs report before the Federal Reserve’s November meeting showed that 263k jobs were added in September, bringing the unemployment rate back down to 3.5%.

- ISM Manufacturing and Services PMIs indicate that demand for goods is slowing swiftly, while demand for services is slowing more gradually and has yet to yield substantial ground.

- Oil supply reductions signaled by OPEC+ this week will raise energy prices (see commentary), creating another headache for the Federal Reserve.

More Jobs, Less Oil, No Pivot

The first week of the third quarter was largely centered around labor market conditions and their potential impact on the policy stance of the Federal Reserve at their November meeting in four weeks’ time in financial news. Lower job openings, higher jobless claims, and slowing job growth all provided some evidence of a softening labor market, but a lower unemployment rate and solid wage growth clouded the aggregate outlook. Equity markets rallied to start the week with hopes of a ‘Fed pivot’ before retreating on Friday as the jobs report drove yields higher and dampened the prospect of a less aggressive Fed. As of the time of writing, the S&P 500 is still up 2.5% for the week, while the ten-year treasury yield sits at 3.9% – 10bps higher than it was to start the day.

The first week of the third quarter was largely centered around labor market conditions and their potential impact on the policy stance of the Federal Reserve at their November meeting in four weeks’ time in financial news. Lower job openings, higher jobless claims, and slowing job growth all provided some evidence of a softening labor market, but a lower unemployment rate and solid wage growth clouded the aggregate outlook. Equity markets rallied to start the week with hopes of a ‘Fed pivot’ before retreating on Friday as the jobs report drove yields higher and dampened the prospect of a less aggressive Fed. As of the time of writing, the S&P 500 is still up 2.5% for the week, while the ten-year treasury yield sits at 3.9% – 10bps higher than it was to start the day.

Non-farm payrolls capped the week, coming in slightly above market expectations with 263k jobs added in September. The unemployment rate ticked down by 0.2 percentage points, back to its July low of 3.5% as the labor force was virtually unchanged from its August level. Combined with steady growth in average hourly earnings of 0.3% month-over-month (m/m), it is clear that the labor market remains strong – a sentiment that is not lost on financial markets which are now pricing in a fourth 75bps hike by the Fed in November with 80% probability.

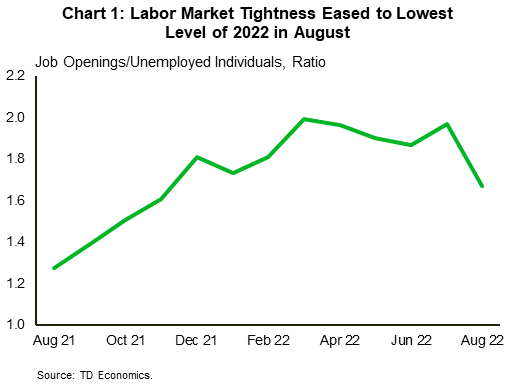

Earlier in the week, we saw job openings for August decline by 10% to reach their lowest level since June 2021. This brought the ratio of job openings to unemployed individuals down to 1.67 – its lowest level since November 2021 (Chart 1). This will be welcomed by Jerome Powell who noted that this ratio was exceptionally high in his September press conference. Jobless claims also displayed signs of softening with a 15.3% increase last week, although this only brings the level of claims back to where it was a month ago. On aggregate, the labor market will need to soften further in order for inflation to sustainably return to the Fed’s target range.

Earlier in the week, we saw job openings for August decline by 10% to reach their lowest level since June 2021. This brought the ratio of job openings to unemployed individuals down to 1.67 – its lowest level since November 2021 (Chart 1). This will be welcomed by Jerome Powell who noted that this ratio was exceptionally high in his September press conference. Jobless claims also displayed signs of softening with a 15.3% increase last week, although this only brings the level of claims back to where it was a month ago. On aggregate, the labor market will need to soften further in order for inflation to sustainably return to the Fed’s target range.

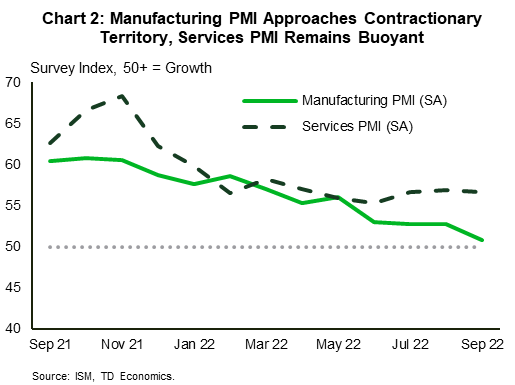

One sector which is showing clear signs of slowing is manufacturing, with the ISM Manufacturing PMI quickly approaching contractionary territory (Chart 2) in financial news. The index dropped by 1.9 percentage points to 50.9 in September, reaching its lowest level since May 2020. Slowing demand was a leading contributor to the lower reading, with both new orders and new export orders contracting. Some of this demand has shifted into the service sectors, with the ISM Services PMI remaining well in expansionary territory, though it too is showing some signs of slowing. While the reading for September was slightly above expectations at 56.7, a slowdown in the backlog of orders as well as new orders could be indicative of the early signs of peak demand for services.

International events this week will serve to further complicate the Fed’s already difficult position, with OPEC+ signaling that it will curtail oil production by 2 million barrels-per-day (bpd). National gas prices, which have been rising for the past few weeks, will likely rise further and return to making positive contributions to headline inflation. Next week’s CPI data for September will provide a better picture of recent developments on the prices front, but as it stands now the Fed will likely remain resolute in its current hawkish stance.

Andrew Foran, Economist | 416-350-8927

This Financial News report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this financial news report has been drawn from sources believed to be reliable but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.

To see more news reports, click here.