FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- China responded to the threat of additional U.S. tariffs by halting agricultural purchases and allowing its currency to weaken beyond the psychologically important 7 yuan to the dollar level.

- Central banks around the world responded to the heightened risk posed by the spiraling trade war by proactively cutting policy interest rates.

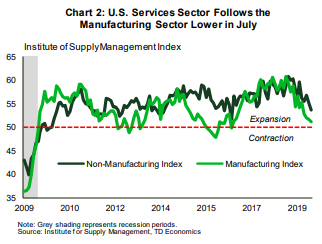

- The U.S. services sector showed signs of cooling in July as the ISM non-manufacturing index declined to 53.7 from 55.1 the previous month.

As U.S. and China Dig in, Central Banks Ease

Heightened U.S.-China trade tensions continue to occupy the limelight. The fallout from last week’s Chinese tariff announcement by President Trump reverberated through the global economy. Last week, the President announced that the U.S. would be imposing a 10% tariff on the remaining Chinese imports previously untouched by tariffs starting September 1st. In response to the tariff threat, China’s currency weakened this week to below the psychologically important level of 7 yuan to the dollar. China also suspended purchases of U.S. agricultural products and has not ruled out placing tariffs on some U.S. imports.

Following the yuan’s depreciation, the U.S. Treasury Department officially designated China a currency manipulator. The action, though mostly symbolic, requires the U.S. to consult with the IMF to try to eliminate any unfair advantage for China from currency manipulation, and could result in further tariff increases in the future.

Amid the growing trade worries, three central banks in the Asia-Pacific region (India, Thailand, New Zealand and the Philippines) proactively lowered interest rates this week. These actions are consistent with the expectation that the global rate-cutting cycle will intensify in the months ahead as the U.S. and China dig in for an extended battle. Meanwhile, despite the Fed delivering on an insurance rate cut last week, the market continues to expect further cuts in September as odds of a recession lurch higher.

Shernette McLeod, Economist | 416-415-0413

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.