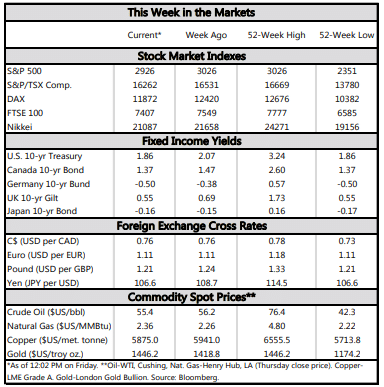

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Financial markets plunged after mixed messaging by the Federal Reserve, and later a 10% tariff on all remaining imported Chinese goods was announced to take effect in September.

- The Federal Reserve cut its policy rate by 25 basis points this week, but markets were unhappy with the lack of commitment to cut more if necessary.

- Slowing global economic growth and past tariff actions suggest that another cut is likely in September. However, escalating trade tensions may require even lower interest rates to help cushion the fallout.

The Fed is Not Done Cutting Rates

Tackling these two events separately, financial markets wanted more clarity on the Fed’s commitment to further rate cuts. First off, many were puzzled as to why rates were cut at all given the solid performance of the U.S. economy. The data this week confirmed that global developments had yet to take a significant toll on domestic economic activity. July payrolls came in as expected, with 164k jobs created, and wage growth firmed up slightly to 3.2% y/y. What’s more, consumer spending for June expanded at a healthy pace, and core inflation registered a slight improvement. Lastly, although motor vehicle sales slowed to a 16.9 million annual pace in July, this remains in line with expectations for 2019 as a whole.

The reason why the Fed is cutting is simple. The data reflects past performance, and forward-looking surveys offer a slightly less favorable outlook. For example, July’s ISM manufacturing survey again edged down and is close to tipping into contraction. Moreover, growth in world GDP is strongly correlated with domestic business investment with a short lag (Chart 1). As a result, the half-point decline in global growth since last year has weighed on business investment enough to shave about a tenth of a point off U.S. growth.

With no end in sight for trade tensions, any larger-than-anticipated negative impact on consumer spending, confidence and business investment would likely call for even lower interest rates to help support U.S. economic growth.

Fotios Raptis, Senior Economist | 416-982-2556

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.