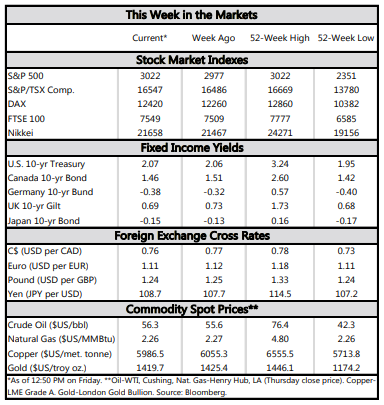

FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Markets had no summer vacation this week, with a new British PM, dovish message from the European Central Bank, and new U.S. GDP data to digest.

- Advanced economy central banks are all sounding dovish, with the Bank of England likely to be more cautious next week now that the risks of a disorderly Brexit have risen.

- Second quarter GDP data showed that U.S. domestic growth remained solid in Q2. But the Fed is likely more concerned with weakness in investment and exports as it prepares to cut rates next week.

Summertime and the Policy’s Easy

Former London mayor Boris Johnson is now Britain’s Prime Minister. Johnson faces an Oct 31st deadline to either leave the EU under the terms of the agreement negotiated by Theresa May, or face a disorderly exit without a deal. The EU had agreed that a UK election would trigger an automatic extension to this deadline, but so far the new PM says an election is off the table. How PM Johnson threads the needle on this one remains to be seen, but it is likely to be a wild ride similar to this past spring. Overall, the odds of a hard Brexit have ticked up in the last two months, and we expect the Bank of England to step back from a hiking bias at its decision next week.

The European Central Bank also hinted at easier monetary policy ahead. Further data this week pointed to a sagging European economy in the second half of the year. Consumer and business confidence have not rebounded from lows consistent with past recessions. Morever, the slump in manufacturing activity is broadening into other regions and industries. This is bad news, as it could trigger a broader pullback on spending, locking in a downward cycle.

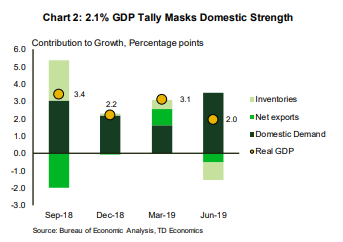

Today’s GDP report (Chart 2) showed that second quarter growth was supported by strong consumer spending. But, the Fed is likely most concerned about the slowdown in investment and the weakness in exports. For now, the consumer is strong enough to keep economic growth sturdy. And now the U.S. economy looks to get a helping hand from Washington. Congress recently agreed to suspend the debt ceiling until after the next election, and raised the spending caps, removing a key fiscal risk this fall. In fact, spending has been raised slightly higher than we assumed in our forecast, presenting a slight upside risk to growth in 2020.

Monetary policy is set to get a little easier both in the U.S. and abroad, and now U.S. fiscal policy is looking a little easier too. These factors should support growth heading into 2020 just as it was starting to look like the edges of the expansion were fraying. This seems to have put markets in a relaxed mood, just in time for summer vacations.

Leslie Preston, Senior Economist | 416-983-7053

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.