FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Chinese economic growth slowed 6.2% y/y in the second quarter of this year, as rising trade tensions weighed on activity. Signs of wear are also showing in the U.S., where industrial output continued to grow at a slow pace in June.

- U.S. housing data remains soft. Starts eased in June, while permits dropped precipitously (-6.1% m/m), pointing to more weakness in the pipeline. That said, the services side of the economy continues to hold up well, with consumption providing a major helping hand. Retail sales rose by 0.4% in June, extending the winning streak to four straight months.

- The resilience of the American consumer suggests less urgency for the Fed to cut rates later this month. But, Fed speakers pushed back against that notion this week, emphasizing the need to get ahead of any potential weakness.

Resilient Consumer Unlikely To Change Fed’s Mind

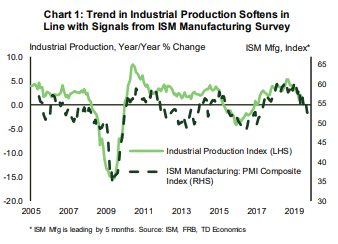

The trade blows are inflicting wounds on both sides. Figures out this week showed that Chinese economic growth slowed to 6.2% year-on-year – the slowest pace in 27 years, with output in secondary industries (construction and manufacturing) decelerating to 5.6% from 6.1% in the first quarter. In the U.S., industrial output continued to grow at a slow pace in June, in line with signals from the ISM manufacturing survey (Chart 1). The impact of the trade conflict is not confined to manufacturing. An annual NAR survey showed that Chinese home purchases in the U.S. fell by 56% in the 12-months ending in March.

Housing data, on the other hand, remains soft. Starts edged lower in June (-0.9%) and have generally moved sideways in recent months. Building permits, however, fell precipitously on the month (-6.1% m/m), suggesting some weakness is still in the pipeline. Despite a favorable demand backdrop and relatively low and falling interest rates, new construction is struggling to kick into higher gear. A lack of buildable lots, labor shortages and increased production costs remain key hurdles.

Looking past housing challenges, the resilience of the American consumer suggests less urgency for the Fed to cut rates later this month. However, several Fed speakers pushed back against that notion this week, emphasizing the need to get ahead of any potential weakness. Still, should the data continue to hold up, the case for limited stimulus (i.e. only 1-2 cuts) is likely to prevail.

Admir Kolaj, Economist | 416-944-6318

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.