FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- The U.S. and China reached a partial trade deal. The U.S. will reduce tariffs from 15% to 7.5% on $120 billion of Chinese imports and cancel the tariffs that were to be imposed on December 15th. In exchange, China will increase its imports of U.S. goods and services.

- American consumption remains healthy. While retail sales were soft in November, spending on services continues to be robust, leaving consumption tracking at 2-2.5% for the fourth quarter of 2019.

- The Conservative party won a majority in the UK election, paving the way for Brexit in January 2020. The next step of securing a trade deal with the EU will likely be more challenging.

Partial Trade Deal Cuts Tariffs

Details of the deal are still to come, but the Office of the United Stated Trade Representative stated that the U.S. will reduce tariffs from 15% to 7.5% on $120 billion of Chinese imports and cancel the tariffs that were to be imposed on December 15th. In exchange, China will substantially increase its imports of U.S. goods and services. We do not have any official figures on this, however. It is quite possible, that this “deal” is a head fake.

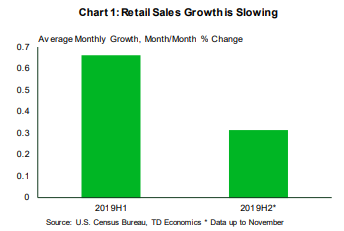

For the time being, with tariffs on Chinese consumer goods now off the table, U.S. retailers will be breathing sighs of relief, especially as retail sales growth has been slowing recently (Chart 1). Indeed, November data, released today, showed retail sales advanced by a soft 0.2% on a month-on-month basis. While spending on goods took a step down, consumption in services was buoyant in the third quarter. The Quarterly Services Survey had revenues in the services sector growing by 5.8% annualized. Overall, these data imply that consumption continues to drive the U.S. economy forward.

Even with all the vibrancy in spending, price pressures are muted. Consumer price inflation in November increased to 2.1% year-on-year from 1.8% in October, but this was mainly due to energy prices. Stripping out energy and food prices, core price inflation remained steady at 2.3%. Past tariffs, too, appear to be not have been fully passed through to consumers. This can be attributed to U.S. retailers absorbing higher prices, as well as a rising U.S. dollar (Chart 2).

The Conservative Party won a resounding majority in the United Kingdom election. With this result in hand, Prime Minister Boris Johnson should be able to lead the country out of the EU. Anticipating this outcome, the pound appreciated, and UK bond yields moved higher. But leaving the EU is only the first hurdle. Next on the agenda is for the parties to agree on a trade deal. This will likely lead to a messier second chapter of the Brexit saga (see commentary).

The end game on Brexit and the China-U.S. trade war remains uncertain. Even what seems like progress towards unwinding uncertainty, reveals more uncertainty. This will continue to be one of the key forces influencing the global outlook in 2020.

Sri Thanabalasingam, Economist | 416-413-3117

Financial News- December 13, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.