FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A Trade tensions reemerged this week. President Trump suggested that the U.S.-China deal could wait until after the election, announced steel and aluminum tariffs on Brazil and Argentina, and threatened to impose tariffs on France. International trade numbers were also unambiguously weak in October, even as trade deficit had narrowed.

- Despite uncertainty on the trade front, it was another banner month for America’s job market. Payrolls rose by a healthy 266k in November, with service sector hiring accelerating for the fourth consecutive month.

- Contraction in the manufacturing sector deepened slightly in November, with the ISM manufacturing index edging lower to 48.1 from 48.3. Service industries continued to expand, alas at a slightly slower pace than in a month prior.

Hiring Remains Solid Despite Trade Tensions

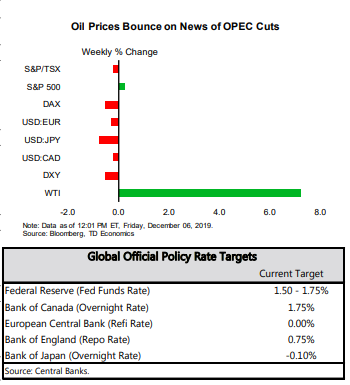

Equity markets rebounded toward the end of the week, amid news of Beijing reaffirming that the talks remain on track and the excellent job numbers. Oil prices rallied on the news that OPEC+ countries agreed to deepen existing production cuts, and Saudi Arabia promising to maintain its voluntary 400K bpd cut, bringing total cuts to 2.1 million bpd.

Trade data was not encouraging this week as trade volumes continued to slow in October. Export and import volumes declined for the second straight month. Since imports fell more than exports the U.S. trade deficit narrowed for the second month in a row, hardly a sign of health.

The services sector hasn’t been immune to trade-related headwinds, with the ISM non-manufacturing index edging 0.8 points lower to 53.9 in October. However, it remains well in expansionary territory, supported by resilient domestic demand. Two-thirds of non-manufacturing industries surveyed in October reported growth, compared to less than a third in the manufacturing survey (Chart 1).

This divergence of fortunes between the manufacturing and services sector continues to manifest in employment data. Payrolls expanded by an impressive 266k in November, with service industries contributing 206k to the headline. Businesses in the services sector have been ramping up hiring since July (Chart 2), while gains remain muted in the goods-producing sector, with the pop in November reflecting the end of the GM strike.

All in all, despite uncertainty on the trade front and softer global growth, the labor market has remained remarkably resilient. With reports like this, the FOMC can sit comfortably on the sidelines after cutting rates three times this year. As long as international risks do not intensify and hurt confidence domestically, the American economy will remain in expansion, supported by a healthy consumer.

Ksenia Bushmeneva, Economist | 416-308-7392

Financial News- December 6, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.