FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- A quiet, holiday-shortened week featured data that painted a picture of an economy that has slowed, but not stalled. Revisions to Q2 GDP did little to change the picture of the economy.

- Durable goods orders were a bright spot, but the Fed’s manufacturing surveys continue to point to a lack of confidence on investment spending. The Beige Book echoed this two-speed view of struggles in the factory sector, and health elsewhere.

- The consumer remains an area of strength, with spending on track to put in a solid performance in Q4, helped by healthy advances in wages and salaries and benign inflation.

Something To Be Thankful For

Final domestic demand was 2% in Q3, after averaging 2.7% in the first half of the year, and 3% in 2018. That is the narrative right there. The economy has slowed from a robust pace to a moderate pace, very close to what we consider its underlying “trend”(Chart 1). The Fed’s latest Beige Book indicated that this tempo has likely continued this quarter. It characterized economic activity as progressing at a modest pace through most districts, unchanged relative to the prior report. Consumer related sectors, including residential construction, are doing well, while ongoing struggles in the manufacturing sector continued.

Durable goods orders for October painted a slightly better picture. Nondefense capital goods orders ex-aircraft, a key signpost to business investment, had a solid gain for the first time in a few months. It wasn’t enough to change our view of manufacturing weakness, but it did support an upgrade to expectations for equipment spending in Q4. Overall, we expect business investment to advance roughly 2.4%, ending two quarters of contraction. However, this does not entirely lift the damper uncertainty is having on investment (see report). Looking at the regional Fed manufacturing surveys, the capital expenditures components on the whole weakened further in November, so we don’t believe business spending or the manufacturing sector is out of the woods yet.

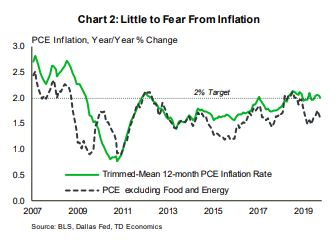

The Fed’s preferred inflation measure – the core PCE deflator – rose only 0.1% in October (Chart 2). The Dallas Fed’s trimmed mean (which strips out price volatility more broadly than food and energy) has been steady at the Fed’s 2% target for a few months. There’s little on the inflation front to spook the Fed to either cut or raise interest rates any time soon. Early in the week, Chair Powell highlighted the benefits of extending the current economic cycle – mainly that lower income households have not yet regained the wealth lost in the great recession. Strong labor markets are finally starting to spark healthy wage gains for lower-income workers, which spreads the gains from a strong economy more broadly. Amid all the trade gloom and uncertainty, that is something to be thankful for.

Leslie Preston, Senior Economist | 416-983-7053

Financial News- November 29, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.