FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- Stocks were volatile this week amid signs that U.S.-China trade talks may be stalling. Cautious optimism briefly returned on Friday on news that the Chinese president was calling for the two sides to “strengthen communication”.

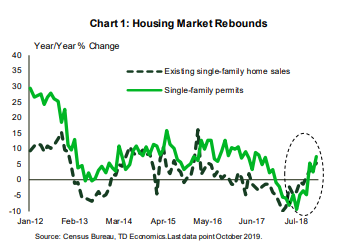

- The housing data released this week was uniformly upbeat. Both construction (+3.8% m/m) and resale activity (+1.9% m/m) picked up in October, suggesting that the housing market was responding nicely to lower mortgage rates.

- The FOMC minutes revealed that most participants judged that three rate cuts left monetary policy sufficiently accommodative to meet the Fed’s objectives, suggesting the Fed is putting back on its “data-dependence” hat.

Housing Market Remained A Bright Spot in October

On the demand side, home sales continued to push higher, rising in three of the past four months as lower mortgages rates boosted affordability. In October, the National Association of Realtor’s affordability metric posted its strongest reading since the end of 2017 – a welcome development for prospective home buyers. That being said, without an equivalent response on the supply side, the latest improvement in affordability might prove fleeting. The already-low inventory of houses on the market has been declining year-over-year for four straight months. This has stymied additional activity and pushed home prices higher, with median home prices up 6.2% from a year ago – a significant acceleration from the roughly 3.5% pace seen at the start of the year.

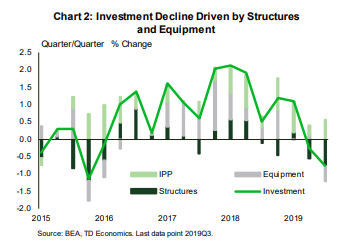

While the housing market has recently emerged as a bright spot, business investment has been a drag on growth. Since last year businesses have found themselves in a deep fog of economic uncertainty brought about by volatile policy making and the U.S.-China trade war, making them reluctant to commit to new investment projects. As we discuss in our recent report, equipment spending – the largest component of business investment – has borne the brunt of the uncertainty impact (Chart 2), with the rise in uncertainty reducing equipment investment by an estimated 4% from 2018Q1 to 2019Q3. The resolution of the trade war could help boost investment. However, a sustained improvement will only be possible once firms are convinced that policy-making will not be as volatile as it has been over the last few years.

The minutes of the FOMC meeting last month revealed that members were also not expecting a quick turnaround in business investment, stating that “trade uncertainty and sluggish global growth would continue to dampen investment spending and exports.” Furthermore, officials have noted that while risks remained “tilted to the downside”, monetary policy was sufficiently accommodative to support outlook of “moderate growth, a strong labor market” and inflation near 2% target following three rate cuts this year. Thus, with regard to future monetary policy, the Fed is putting back on its “data-dependence” hat, and only a material change in the economic outlook will move it off the sidelines.

Ksenia Bushmeneva, Economist | 416-308-7392

Financial News- November 15, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.