FINANCIAL NEWS HIGHLIGHTS OF THE WEEK

- U.S. data this week showcased the contrasting feature of the U.S. economy: a resilient U.S. consumer but a struggling manufacturing sector.

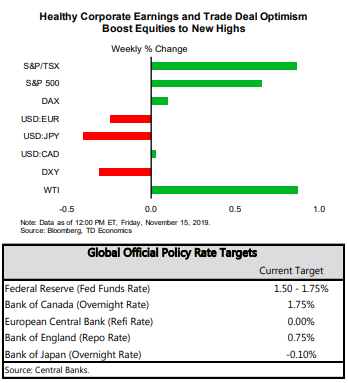

- Negotiations on a phase one trade deal between the U.S. and China took a step back this week as negotiators struggled to come to a compromise. A deal is unlikely to be signed before the end of this month.

- Inflation remained subdued as the high dollar, inventory stockpiling and margin compression offset the price increases implied by tariffs.

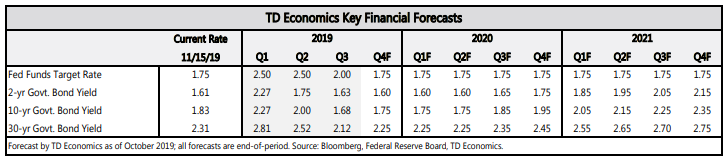

- With the economy evolving in line with their view, we believe the Fed has completed its mid-cycle adjustment.

Consumers Resilient Amid Manufacturing Struggles

Retail sales data released today showed that spending bounced back from a dip in September. Sales at non-store retailers, which includes online sellers, drove the increase. With the job market strong and consumers continuing to see solid gains in wages, consumption should remain healthy through the remainder of the year.

The manufacturing outlook isn’t as bright. Newly released production data indicated that manufacturing took another step down in October (Chart 1). The U.S.-China trade war and softer global economic conditions are clearly weighing on the sector. However, as noted in a recent report, it is unlikely that, the malaise in manufacturing can single-handedly trigger a recession, given its small and shrinking share of the U.S. economy.

Although manufacturing weakened, we saw some improvement in small business confidence. The NFIB small business optimism index increased in October, with businesses signaling they will move forward with capital outlays in the months to come. This is a good sign for sputtering investment, which has contracted in the last two quarters as economic policy uncertainty spiked (Chart 2).

Much of this increase in uncertainty is coming from the U.S.-China trade war. There was some optimism last week that we might see the first deal in the conflict as the two sides edged towards a phase one mini-deal. It was even reported that the deal might be made official before the end of this month. However, it’s probably too early to pop the champagne. News emerged this week that officials were struggling to complete the deal. According to reports, China wants a greater reduction in tariffs, while U.S. officials do not believe China has made enough concessions to justify their removal. It’s probably a good idea to not hold our breath as we await the first breakthrough in this drawn-out saga.

Although trade uncertainty has made its way through the U.S. economy, it has yet to show up in overall price pressures. Indeed, despite the imposition of tariffs on many imported consumer goods from China in September, goods prices, which bear the brunt of the tariffs, on aggregate only rose by 0.3% on a year-over-year basis.

In addition to the rising U.S. dollar, other forces may be counteracting the price increases implied by tariffs. Elevated inventories for some consumer products are likely putting downward pressure on prices. There are also indications that importers are absorbing tariff impacts by compressing margins. The latter demonstrating how some U.S. firms are shouldering the burden of the trade war.

From the Federal Reserve’s perspective, the data are evolving largely in line with their economic forecasts. Inflation is at target and the consumption remains healthy. In addition, past rate cuts are moving through the economy, with the impacts most noticeable in housing. As we stated in an earlier report, without any further negative shocks, we believe the Fed has completed its mid-cycle adjustment.

Sri Thanabalasingam, Economist | 416-413-3117

Financial News- November 15, 2019

This report is provided by TD Economics. It is for informational and educational purposes only as of the date of writing, and may not be appropriate for other purposes. The views and opinions expressed may change at any time based on market or other conditions and may not come to pass. This material is not intended to be relied upon as investment advice or recommendations, does not constitute a solicitation to buy or sell securities and should not be considered specific legal, investment or tax advice. The report does not provide material information about the business and affairs of TD Bank Group and the members of TD Economics are not spokespersons for TD Bank Group with respect to its business and affairs. The information contained in this report has been drawn from sources believed to be reliable, but is not guaranteed to be accurate or complete. This report contains economic analysis and views, including about future economic and financial markets performance. These are based on certain assumptions and other factors, and are subject to inherent risks and uncertainties. The actual outcome may be materially different. The Toronto-Dominion Bank and its affiliates and related entities that comprise the TD Bank Group are not liable for any errors or omissions in the information, analysis or views contained in this report, or for any loss or damage suffered.